Embarking on the journey of higher education is an exhilarating experience, but it often comes with the daunting challenge of managing student loan debt. While securing loans might seem like the only path to achieving your academic goals, there are creative strategies to tackle this financial burden even before you toss your graduation cap into the air. Let's explore some innovative approaches to minimize student loan debt while you're still navigating through college.

Optimize Your Course Load and Graduate Early

The traditional four-year college timeline isn't set in stone. By optimizing your course load, you can potentially graduate sooner and save on tuition costs. Taking extra credits each semester or enrolling in summer courses can accelerate your graduation timeline. This not only reduces the amount of time you're accruing fees but also allows you to enter the workforce earlier, starting your earning and repayment period sooner.

Is Graduating Early Right for You?

Considering graduating early as a strategy to reduce student loan debt? Take this interactive quiz to find out if this option aligns with your educational goals and circumstances.

Additionally, Advanced Placement (AP) classes and community college courses taken during high school can often be transferred for credit, shaving off time and money from your university experience. It's essential to consult with your academic advisor to ensure that these credits will be accepted by your institution.

Leverage Work-Study Programs or Part-Time Jobs

Balancing work and study might seem challenging, but it's a practical approach to offset some of the costs associated with college. Federal Work-Study provides part-time jobs for undergraduate and graduate students with financial need, allowing them to earn money that can be used for education expenses. The beauty of work-study programs is that they are typically flexible around student schedules and located on or near campus.

Top Work-Study Jobs

- Library Assistant - Help manage library resources and assist students, averaging around $12/hour.

- Research Assistant - Support faculty with academic research, typically earning $13-$15/hour.

- Teaching Assistant - Assist professors with classes and grading, with pay usually between $13-$16/hour.

- IT Support Helpdesk - Provide tech support to students and staff, often paid at $12-$14/hour.

- Administrative Assistant - Work in various university offices, handling clerical tasks for an average of $12/hour.

- Student Event Coordinator - Plan and execute campus events, typically earning around $11-$14/hour.

- University Bookstore Clerk - Manage sales and stock at the campus bookstore, with an average wage of $10-$13/hour.

- Residence Hall Advisor - Supervise and support students living on campus, usually compensated with room and board plus a stipend.

- Peer Tutor - Tutor fellow students in subjects you excel in, often paid $10-$15/hour.

- Campus Tour Guide - Lead prospective students and visitors around campus, typically paid $10-$12/hour.

If work-study isn't available or sufficient, consider part-time jobs or freelancing opportunities related to your field of study. Not only does this provide income, but it also grants valuable experience that could make you more marketable upon graduation.

Apply for Scholarships and Grants Relentlessly

Scholarships and grants are essentially free money – they don't need to be repaid! Exhaust every avenue here by applying for as many as possible, no matter how small they may seem. There are scholarships based on merit, sports ability, artistic talent, or even unique personal characteristics or interests.

The key is persistence and not being discouraged by rejections. Utilize scholarship databases, school resources, community organizations, and even social media channels to uncover opportunities. Remember that every dollar earned through scholarships is one less dollar borrowed.

Cut Down Expenses with Budgeting

Mindful budgeting during your college years can significantly impact the amount of debt you accumulate. Start by tracking all expenses for a month – this will give you a clear picture of where your money goes. Then set a realistic budget that prioritizes needs over wants.

Consider cost-saving measures like buying used textbooks, opting for cheaper housing options such as shared apartments instead of dorms, cooking meals at home rather than eating out frequently, and taking advantage of student discounts whenever possible.

In conclusion (but not really since we're just getting started), remember that tackling student loan debt while in school isn't about making one big gesture—it's about making many small ones that add up over time. Stay tuned as we delve deeper into more strategies such as side hustles tailored for students, understanding loan interest rates better through our proven strategies guide, and exploring loan forgiveness programs in the second half of this article.

Freelancing and Side Hustles

With the gig economy booming, students are finding innovative ways to earn money that can be put towards their student loan debt. Freelancing platforms like Upwork or Fiverr offer a multitude of opportunities for students to leverage their skills. Whether it's graphic design, writing, coding, or tutoring, there's a side hustle out there for everyone. The key is to find a balance that allows you to both excel in your studies and manage your freelance work effectively.

Remember, the income from side hustles doesn't just have to go towards living expenses; it can be a strategic way to make extra payments on your student loans. This can significantly reduce the amount of interest that accrues over time, saving you money in the long run.

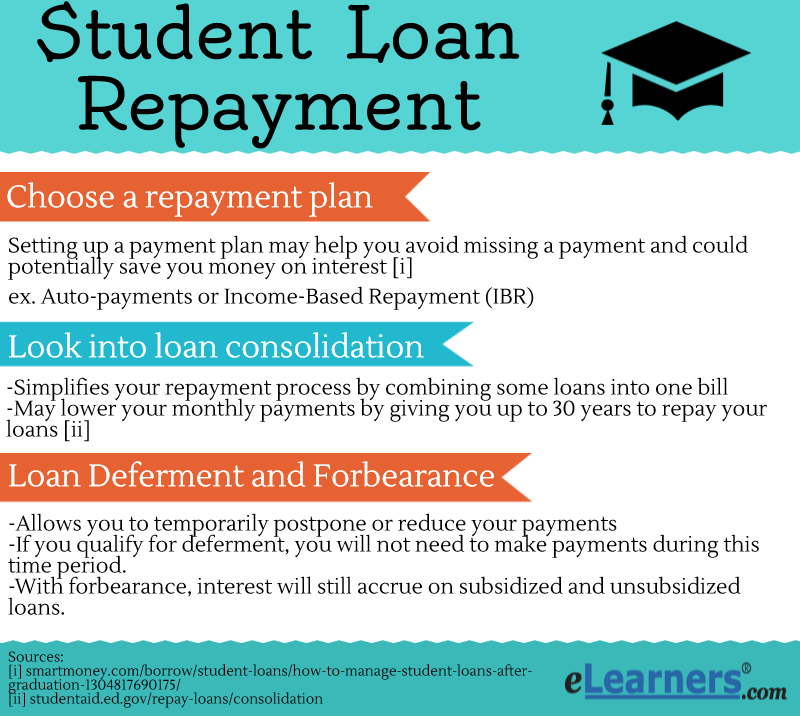

Understanding Repayment Plans

While still in school, it’s essential to understand the different repayment plans available. Federal student loans offer several repayment options that can be tailored to fit your financial situation post-graduation. Plans based on income are particularly useful for those who might not secure high-paying jobs immediately after college.

Mastering Your Student Loan Repayment Strategy

Understanding your student loan repayment strategy is essential while you're still in school. This quiz will help you assess your knowledge and prepare for the financial responsibility that comes with student loans.

Income-driven repayment plans, for example, adjust your monthly payments according to your income level and family size. Familiarizing yourself with these plans now will prepare you for making wise decisions when it's time to start repaying your loans.

Applying for Scholarships and Grants

Scholarships and grants are essentially free money that you don't have to pay back—making them an excellent way to reduce future loan debt. Many students believe they aren't eligible for scholarships after their freshman year, but this is a myth. There are countless opportunities throughout your college career; it just takes dedication and effort to search and apply for them.

Unlocking Opportunities: Your Guide to Scholarship Success

Universities often have resources available to help students find scholarships and grants they may qualify for. Additionally, online databases provide extensive lists of awards available based on various criteria such as field of study, background, or unique talents.

"Every dollar earned through scholarships is a dollar less borrowed. It pays off exponentially in reducing future debt burdens."

Creative Budgeting and Saving Strategies

Budgeting may not sound like the most exciting strategy, but it's a powerful tool in managing finances effectively—even while still in school. Apps like Mint or YNAB (You Need A Budget) can help track spending habits and identify areas where you can cut back. Small changes in daily spending habits can add up over time and allow you to make additional loan payments.

Top Budget Apps for Students

- Mint - Effortlessly manage your finances and track your loans in one place.

- You Need A Budget (YNAB) - Embrace a proactive budget philosophy tailored for students.

- PocketGuard - Simplify budgeting with an app that helps prevent overspending.

- Goodbudget - Utilize the envelope budgeting system digitally to control your spending.

- EveryDollar - Plan your monthly budget in minutes and stay on top of your student loans.

- Personal Capital - A comprehensive financial tool for a high-level view of your finances, including loans.

- Albert - Get personalized financial advice and optimize your student budget.

- Wally - Take control of your money with intuitive tracking and budgeting features.

Saving might also seem daunting on a tight budget but consider opening a high-yield savings account where you can stash any extra cash from work or gifts. Even if the contributions are small, they'll grow thanks to compound interest—and every little bit helps when tackling student loan debt.

Incorporating these creative strategies into your daily life as a student will not only help manage existing student loan debt but also instill financial habits that will benefit you long after graduation. Always stay informed about strategies to avoid accumulating large amounts of debt and explore ways future college students can avoid student loan debt altogether. Remember that every step taken today towards managing your loans is a leap towards financial freedom tomorrow.

- Quiz: Understanding Student Loans & Avoiding Debt

- Minimizing Student Loan Costs: Proven Strategies

- Managing Student Loans Without Completing Your Degree

- Quiz: Calculate Your Potential Student Loan Debt

- Quiz: Managing Student Loans Without A Degree

- Quiz: Avoiding Student Loan Default & Understanding Loan Acceleration

- Quiz: Determine Your Student Loan Repayment Strategy

- Quiz: Understanding & Managing Student Loan Debt

No comments yet. Be the first to share your thoughts!