Embarking on the journey of higher education can be as exhilarating as it is daunting, particularly when it comes to navigating the seas of student loan repayment. A significant decision that borrowers may face is whether to extend the maturity date of their student loan. But what exactly does this mean, and when might it be a wise choice? Let's dive into the intricacies of loan term extension and unravel when it could be beneficial for you.

Understanding Loan Maturity Dates

A student loan's maturity date is the point in time at which you are expected to have fully repaid your loan. It's a finish line that seems distant at the outset but becomes increasingly significant as you progress through your repayment journey. Knowing when this date is and how it affects your finances is crucial. If you're unsure about your loan's specifics, brush up on your knowledge with our quiz on understanding student loan maturity dates.

Why Consider Extending Your Loan Term?

Life doesn't always go according to plan, and financial situations can change. Perhaps you've encountered unexpected expenses or a shift in income. In such cases, extending your loan term may offer some breathing room by reducing monthly payments, even though it could mean paying more interest over time. To get a clearer picture of how long until your student loan is paid off under different scenarios, visit our guide on understanding loan maturity dates.

The Pros and Cons of Loan Term Extension

Let's break down the advantages and disadvantages of extending your student loan term:

- Lower Monthly Payments: A longer term generally means lower monthly payments, which can ease your budget constraints.

- Increased Flexibility: With more manageable payments, you might find it easier to handle unforeseen financial challenges.

- Potential for Improved Credit: Consistent on-time payments could positively affect your credit score.

However, there are downsides too:

- Total Interest Paid: More months means more interest accrual, increasing the overall cost of your loan.

- Prolonged Debt: An extended term also means you'll be in debt for a longer period.

- Opportunity Cost: The money spent on extra interest could have been invested elsewhere.

To assess whether extending your student loan makes sense for you, consider taking our quiz on understanding student loan terms and conditions.

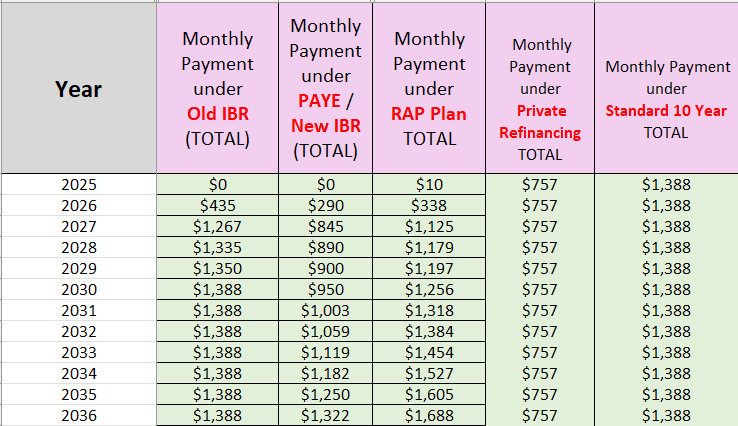

Comparing Long-Term Costs: Standard vs. Extended Repayment Plans

Evaluating Your Financial Goals

Your decision should align with both your immediate budget needs and long-term financial goals. If you aspire to become debt-free quickly or are working towards significant savings goals like buying a home or investing, extending your repayment term might not align with these ambitions. Conversely, if immediate financial relief is paramount to maintain stability or invest in career growth opportunities such as further education or starting a business, then an extension could be justified.

Loan Term Tips

- Monthly Budget - Assess how extending your loan term will impact your monthly budget and cash flow.

- Interest Accumulation - Calculate the total interest you'll pay over the extended loan period compared to your current term.

- Financial Goals - Consider how extending your loan term aligns with your long-term financial objectives, such as buying a home or saving for retirement.

- Current Interest Rates - Evaluate if the current interest rates are favorable for extending your loan term.

- Credit Impact - Understand how the extension might affect your credit score and borrowing capacity in the future.

- Loan Forgiveness Programs - Explore if you're eligible for any loan forgiveness programs that could be affected by changing your loan term.

- Prepayment Penalties - Check for any prepayment penalties that could apply if you decide to pay off your loan early after extending the term.

- Job Stability - Take into account your job security and the likelihood of your income increasing, which could influence the decision to extend your loan term.

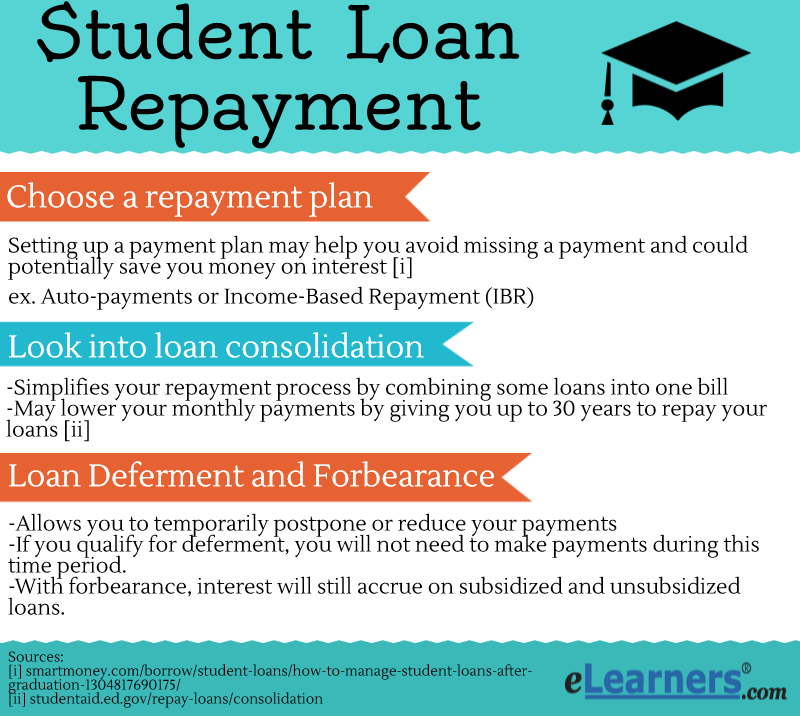

- Alternative Options - Compare the loan term extension with other debt management strategies, such as refinancing or consolidation.

In conclusion, while we've begun to explore why someone might opt for a longer repayment period for their student loans, remember that this decision should be made with careful consideration of individual circumstances. Stay tuned as we delve deeper into strategies for managing an extended loan term effectively and maintaining financial health despite longer repayment periods in the second half of our article.

To further enhance your understanding before making such an important decision, take our comprehensive test on understanding student loans. And remember: informed choices lead to empowered borrowers!

Considerations for Extending Your Loan Term

Extending the term of your student loan can be a double-edged sword. While it may lower your monthly payments, it also means that you'll be paying more in interest over the life of the loan. It's crucial to consider your current financial situation and future income prospects. If you're in a field with rising salary trajectories, you might manage higher payments later on. But if you're not expecting significant income growth, a longer loan term could lead to financial strain.

Understanding Student Loan Term Extensions

Deciding whether to extend the maturity date of your student loan can be a complex decision. This quiz will help you understand when it might make sense to consider a loan term extension.

Remember that extending your loan term is not a decision to be taken lightly. It's important to evaluate the long-term benefits versus the costs. Use our interactive quiz to test your knowledge on how interest rates and loan terms affect your repayment plan.

The Impact of Refinancing on Loan Maturity

Refinancing is another option that can change the maturity date of your student loans. This process involves taking out a new loan with different terms to pay off your existing loans. Refinancing can lead to a lower interest rate or different repayment terms, which might include extending your loan's maturity date.

However, refinancing isn't for everyone. If you have federal student loans, you'll lose access to certain benefits such as income-driven repayment plans and potential forgiveness programs. Before making any decisions, weigh the pros and cons carefully and consider how refinancing will affect your overall financial goals.

Making an Informed Decision

Making an informed decision about extending your student loan term requires understanding all the variables involved. From changes in interest rates to how it affects your total repayment amount, there's a lot to consider.

To get a clearer picture of what extending your loan term could mean for you financially, use our interactive calculators. They can help project future payments and total interest paid over the life of the loan under different scenarios.

If after using these tools you're still unsure about whether extending your loan term is right for you, don't hesitate to seek advice from a financial advisor or explore other resources such as our financial literacy quiz.

In addition to these considerations, staying informed about changes in federal policy regarding student loans is also important. For instance, potential legislation could affect interest rates or offer new forgiveness programs which might influence your decision on whether or not to extend your loan term.

Comparing Long-Term Costs and Savings of Student Loan Term Extension

To sum up, extending the maturity date of a student loan isn't just about making monthly payments more manageable—it's about considering the total cost over time and how it fits into your broader financial plan. With careful planning and access to resources like our site's quizzes and calculators, you can make an educated choice that aligns with both your current budget and future financial aspirations.

For further reading on this topic and related areas like consolidation options or understanding complex terms associated with student loans, explore our comprehensive guides at Need Student Loan. And remember, we're here every step of the way on this journey towards managing—and mastering—your educational debt.

No comments yet. Be the first to share your thoughts!