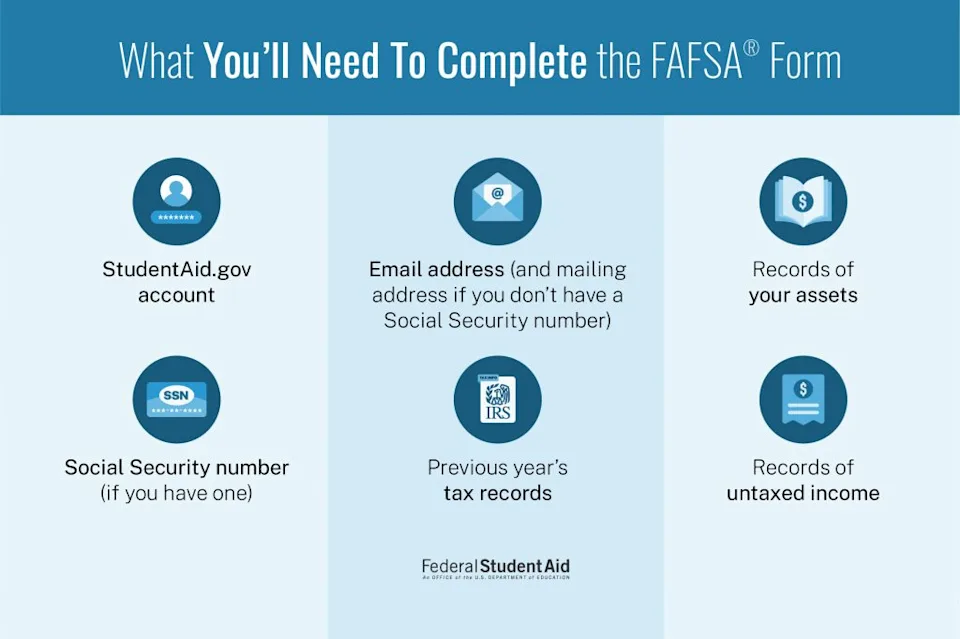

Gather documents before you start

The FAFSA application is essentially a data entry exercise. If you stop to hunt for a tax transcript or a bank statement in the middle of the process, you risk losing your focus or running out of time. The most effective way to secure your aid offer is to have every required document open in a separate browser tab or spread across your desk before you click "Start."

What to collect

The 2026-27 FAFSA form requires specific financial records. For most students, this includes your federal income tax returns, W-2 forms, and records of untaxed income. If you are a dependent student, your parents must provide the same documentation. Unmarried parents or those who are divorced may need to provide information for only one parent, depending on who provided more financial support, but both sets of records should be gathered just in case.

Keep your Social Security numbers, driver's license numbers, and alien registration numbers (if applicable) easily accessible. You will also need a list of the colleges you want to receive your data. Having these school codes ready prevents delays in sending your application to every institution you are considering.

Create your FSA ID early

You cannot complete the FAFSA without an FSA ID, which serves as your legal electronic signature. This is not just a username and password; it is a secure credential that verifies your identity to the federal government. The verification process can take up to three days, so do not wait until the day you plan to submit your application.

Both students and parents (if the student is dependent) need their own separate FSA IDs. The student uses theirs to sign the application, and the parent uses theirs to sign if required. If you are waiting on a parent to create their account, this delay can hold up your entire submission. Set up your accounts at least a few days before the deadline to ensure there are no technical hurdles.

Understand dependency status

Before gathering financial records, confirm your dependency status. This determines whose income and assets you must report. Most undergraduate students under age 24 are considered dependent, meaning they must include their parents' financial information. However, if you are married, a graduate student, a veteran, or have legal dependents of your own, you may be independent.

If you are unsure about your status, use the dependency status questionnaire on studentaid.gov. Getting this right is critical because misreporting your status can lead to an incorrect aid offer or even penalties later. Once you know your status, you can tailor your document gathering to match exactly what the form requires.

Follow the step-by-step application

FAFSA works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Avoid common data entry errors

Small mistakes on the Free Application for Federal Student Aid (FAFSA) can trigger delays or reduce your aid offer. The system relies on exact matches between what you enter and what the government has on file. Even a single wrong character can flag your application for manual review, pushing your award letter weeks behind schedule.

The most frequent errors involve identity and household status. Marital status is often confused with relationship status; you must report your legal status as of the day you submit the form, not your current living arrangement. Similarly, misreporting assets—such as forgetting to include a small savings account or misclassifying a family business—can skew your financial contribution calculation. These fields directly determine how much federal grant and loan money you qualify for.

Another common pitfall is leaving fields blank when the answer is "zero" or "none." The FAFSA treats empty fields differently than explicit zeros. If you do not own a home or have no investments, you must explicitly enter "0" in those boxes. Leaving them blank may cause the form to reject your submission or assume incomplete data, requiring you to restart the process.

To minimize anxiety and ensure accuracy, treat the FAFSA like a tax return: verify every number before moving on. Use the IRS Data Retrieval Tool if available, as it pulls your tax information directly, reducing the chance of manual transcription errors. Double-check your Social Security numbers and dates of birth against your official documents. These steps prevent the most costly delays in the financial aid process.

Report your legal marital status as of the submission date. If you are separated or divorced, this often changes your dependency status and asset reporting requirements.

Include all cash, savings, and investment accounts. Omitting a small account can lead to an incorrect aid calculation and potential repayment issues later.

Never leave a financial field blank if the answer is zero. Explicitly enter "0" to confirm you have no assets or income in that category.

Review the Student Aid Report

Once you submit the FAFSA, the Department of Education sends you a Student Aid Report (SAR). This document is your financial aid receipt, showing the data you provided and the calculated Expected Family Contribution (EFC). For the 2026-27 cycle, this number determines your eligibility for federal grants, work-study, and loans.

Log in to studentaid.gov using your FSA ID to view and print your SAR. Check the EFC figure carefully. If the number seems unusually high or low, it may reflect a data entry error. You can correct mistakes directly on the SAR before the system finalizes your record.

Verify that your school codes are listed and active. If a school is missing or marked inactive, update your FAFSA immediately to ensure they receive your financial data. Without this step, your aid package cannot be processed.

Compare aid offers to lower costs

Financial aid award letters are marketing documents designed to look generous. They often highlight the total package value while burying the loan requirements in small print. To minimize debt, you must strip away the noise and compare the actual cost of attendance against the "free money" and work-study portions.

Start by listing every cost item your school charges: tuition, fees, room, and board. Then, subtract the total of all grants, scholarships, and federal work-study funds. The remaining balance is the amount you will need to cover with loans or personal savings. This net cost figure is the only number that matters for your budget.

When comparing loans, prioritize federal Direct Subsidized and Unsubsidized Loans. These fixed-rate options include borrower protections like income-driven repayment that private lenders rarely match. Only consider private loans if you have exhausted all federal limits and have a co-signer with strong credit.

| Aid Type | True Cost | Repayment Terms | Flexibility |

|---|---|---|---|

| Grants/Scholarships | $0 | None | N/A |

| Federal Direct Loans | Low fixed interest | 10+ year standard | Income-driven options |

| Private Student Loans | Variable or high fixed | Varies by lender | Limited or none |

-

Calculate net cost by subtracting grants from total charges.

-

Prioritize federal loans over private alternatives.

-

Verify work-study availability and expected earnings.

-

Check for hidden fees in private loan terms.

No comments yet. Be the first to share your thoughts!