Federal loan rates for 2026

Federal student loan interest rates go up for the 2026-2027 academic year. Direct Subsidized Loans are 5.5%, Direct Unsubsidized Loans are 6.5%, and Direct PLUS Loans are 8.5%. These rates are higher than last year and affect anyone taking out a new loan after July.

The increase is directly tied to the May 2026 auction of the 10-year Treasury note. Federal student loan rates are calculated by adding a fixed percentage to the 10-year Treasury note rate, and the recent auction resulted in a higher benchmark. It’s understandably frustrating to see rates climb when you’re already thinking about the weight of student debt, but understanding the mechanism behind it is the first step to navigating these changes.

These changes only apply to loans disbursed on or after July 1, 2026. If you already have fixed-rate federal loans, your rate stays the same. You only need to worry about these higher costs for the money you borrow next year.

How the new rates are calculated

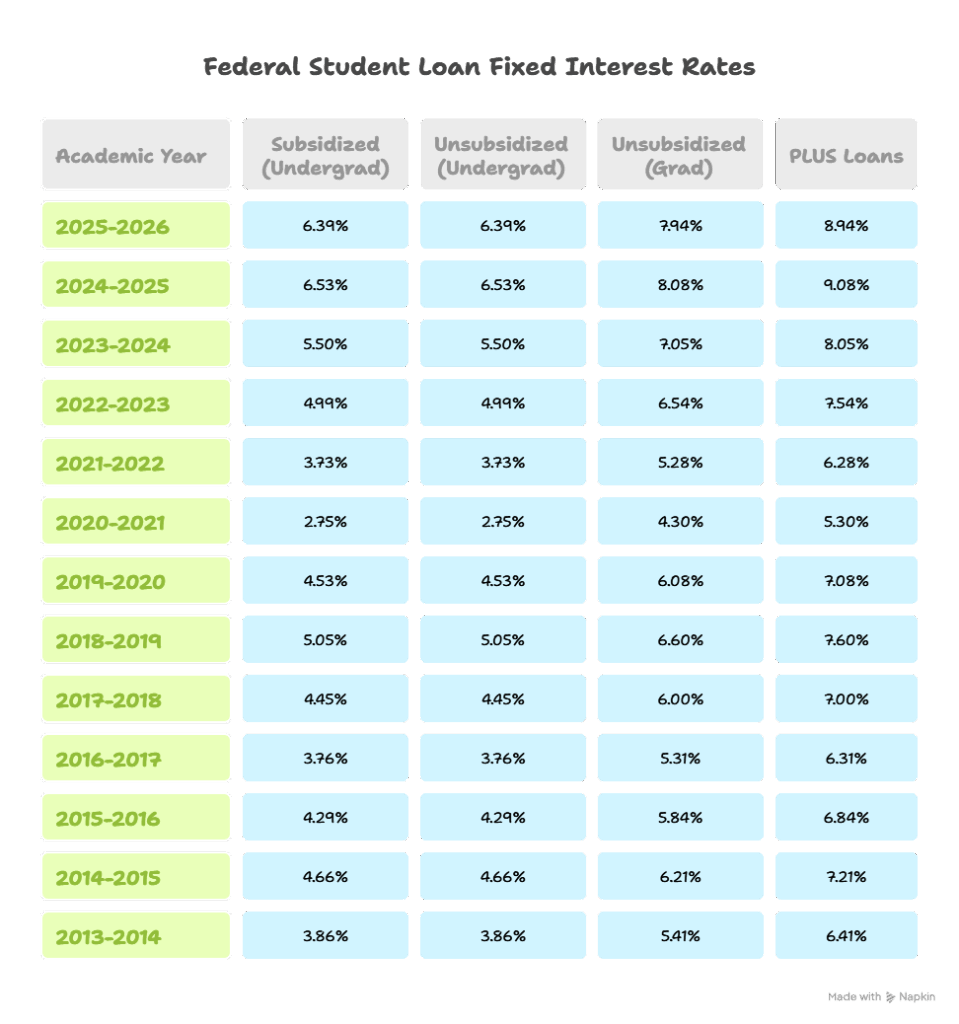

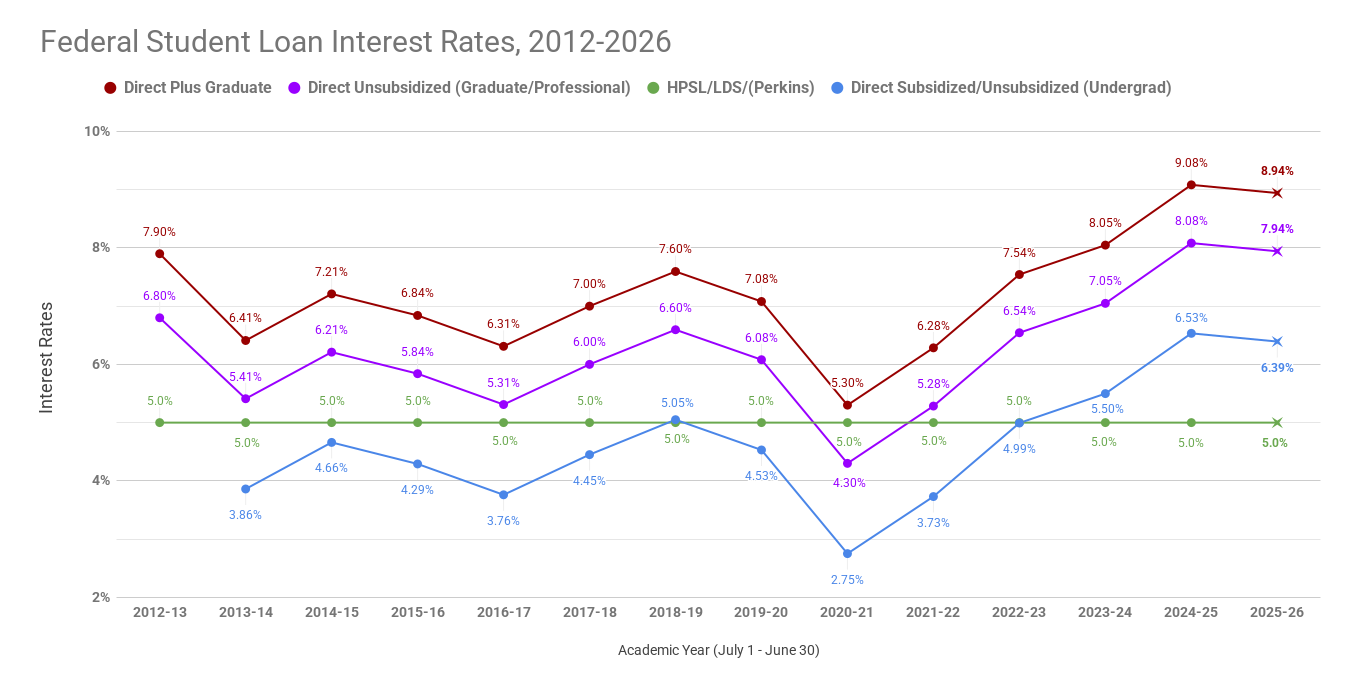

Let’s put these numbers into perspective. In the 2025-2026 academic year, Direct Subsidized Loans were at 5.05%, Unsubsidized at 6.05%, and PLUS loans were 7.05%. That's a half-percent increase for Subsidized and Unsubsidized, and a full percentage point jump for PLUS loans. While seemingly small, these increases add up over the life of the loan.

The calculation is fairly straightforward: Congress sets a fixed percentage that is added to the May 10-year Treasury note rate. For undergraduate Direct Loans, it's currently the 10-year Treasury note rate plus 2.75%. For PLUS loans, it’s the 10-year Treasury note rate plus 3.6%. This means that as the Treasury yield fluctuates, so do the federal student loan rates.

Most federal student loans come with fixed interest rates, offering predictability throughout the repayment period. This is in contrast to variable rate loans, where the interest rate can change over time. Interest also accrues on federal loans, meaning that interest begins to build up from the moment the loan is disbursed, even while you’re still in school. Understanding accrual is important for calculating your total loan cost.

Federal Student Loan Interest Rates (2024-2026)

| Loan Type | 2024-2025 Rate | 2025-2026 Rate | Change (Percentage Points) |

|---|---|---|---|

| Direct Subsidized Loans (Undergraduate) | 5.05% | 5.50% | 0.45 |

| Direct Unsubsidized Loans (Undergraduate) | 5.05% | 5.50% | 0.45 |

| Direct Subsidized Loans (Graduate) | 6.84% | 7.29% | 0.45 |

| Direct Unsubsidized Loans (Graduate) | 6.84% | 7.29% | 0.45 |

| Direct PLUS Loans (Parents & Graduate Students) | 8.05% | 8.50% | 0.45 |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

The impact on parent borrowers

Direct PLUS Loans are often overlooked in these discussions, but the rate increase to 8.5% is particularly significant for parent borrowers. These loans are available to parents of dependent undergraduate students, and also to graduate or professional students. Borrowers can typically borrow up to the cost of attendance, minus any other financial aid received.

Higher rates are a burden for parents. However, PLUS loans are eligible for income-driven repayment (IDR) plans. These plans lower monthly payments based on your income and family size, which helps if the 8.5% rate is too expensive for your budget.

Unlike many other federal loans, PLUS loans do require a credit check. Borrowers must demonstrate a satisfactory credit history to qualify. A negative credit history can prevent a parent from securing a PLUS loan, potentially leaving their child with fewer funding options. This requirement adds another layer of complexity for families.

Estimated monthly payments

Let's look at some real-world examples. If a student borrows $5,000 at the new 5.5% rate for a Direct Subsidized Loan and repays it under the Standard 10-year Repayment Plan, their estimated monthly payment would be around $59. If they borrow $10,000, the payment jumps to $118. For a $20,000 loan, you’re looking at approximately $236 per month.

Now, let’s consider the impact of the PLUS loan rate increase. A $10,000 PLUS loan at 8.5% repaid over 10 years would result in a monthly payment of around $149. It’s important to remember these are estimates, and your actual payment may vary based on your specific loan terms and repayment plan.

Over the life of the loan, even a small interest rate increase can significantly increase the total amount repaid. For example, on a $20,000 loan, a 1% increase in the interest rate could add hundreds or even thousands of dollars to the total cost. It's easy to underestimate this, so carefully consider the long-term implications of borrowing.

Income-driven repayment options

Income-Driven Repayment (IDR) plans can offer a crucial safety net for borrowers facing higher loan payments. These plans base your monthly payment on your income and family size, potentially making your payments more affordable. Several IDR plans are available, including the Saving on a Valuable Education (SAVE) plan, Income-Based Repayment (IBR), Income-Contingent Repayment (ICR), and Pay As You Earn (PAYE).

Eligibility requirements vary depending on the plan. The SAVE plan, for example, generally offers the most generous terms and is available to borrowers with eligible federal student loans. Payments are calculated as a percentage of your discretionary income, and any remaining balance may be forgiven after a certain number of years of qualifying payments. However, forgiven amounts may be taxable.

Navigating the IDR system can be complex. It’s essential to carefully research each plan and determine which one best fits your individual circumstances. The Federal Student Aid website (studentaid.gov) provides detailed information about each plan, eligibility requirements, and an IDR simulator to help you estimate your monthly payments. Don't hesitate to use their resources.

The risks of refinancing

Refinancing your federal student loans with a private lender is another option to explore, particularly if you have a good credit score and a stable income. Refinancing involves taking out a new loan from a private lender to pay off your existing federal loans. This can potentially result in a lower interest rate and simplified repayment.

Refinancing has downsides. You lose access to federal protections like income-driven repayment and loan forgiveness. Once you move to a private lender, those benefits are gone forever. I wouldn't trade federal safety nets for a slightly lower rate unless your income is very stable.

To qualify for refinancing, you typically need a strong credit score and a steady income. The application process usually involves providing documentation of your income, employment, and existing student loan debt. Carefully compare offers from multiple lenders before making a decision, and weigh the potential benefits against the loss of federal protections.

No comments yet. Be the first to share your thoughts!