What is changing for 2026-2027?

The Free Application for Federal Student Aid (FAFSA) is undergoing significant changes for the 2026-2027 academic year. These aren’t minor tweaks; they represent a fundamental shift in how financial aid is determined and distributed. The Department of Education aims to simplify the process and expand access to aid, particularly for low-income students. This overhaul is a direct response to years of criticism about the FAFSA’s complexity and barriers to entry.

At the heart of these changes is a streamlined form with fewer questions. They're also replacing the Expected Family Contribution (EFC) with the Student Aid Index (SAI). This new metric is designed to provide a clearer picture of a student’s ability to pay for college. The changes also involve a greater reliance on direct data exchange with the IRS, which, in theory, should reduce the burden on students and families.

The 2024-2025 rollout was a mess of technical delays and broken forms. The Department of Education says they've fixed those bugs for the 2026-2027 cycle, but we'll see if the system actually holds up under the new data exchange requirements.

These updates change the math for almost every applicant. This guide breaks down the new deadlines and the specific data you'll need to have ready before the application opens.

Shorter forms and IRS data sharing

The 2026-2027 FAFSA will be significantly shorter than previous versions. Many questions about things like untaxed income and assets will be removed. The goal is to reduce the cognitive burden on students and families, making the application process less daunting. This focus on simplification is a welcome change, as the previous FAFSA was often criticized for being overly complex and time-consuming.

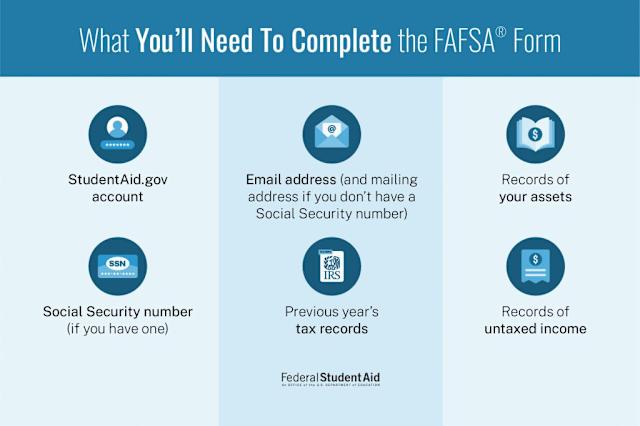

A key component of the simplification is the move towards direct data exchange with the IRS. The FAFSA will directly import tax information for both the student and their parents, eliminating the need to manually enter this data. This should reduce errors and streamline the process. However, it also introduces potential challenges. If there are discrepancies between the IRS data and what the student reports, it could cause delays or require additional documentation.

Students and parents will need to carefully review the data imported from the IRS to ensure accuracy. If there are errors on your tax return, you'll need to amend it before completing the FAFSA. The Department of Education is providing resources to help with this process, but it’s crucial to be proactive. Reporting parental income will also shift, with a greater emphasis on current income rather than historical data.

For students whose parents are self-employed, this data exchange may be more complex. Self-employed individuals often have more complicated tax situations, and it's possible that the IRS data may not accurately reflect their income. In these cases, students may need to provide additional documentation to verify their parents’ income. It’s a good idea to start gathering tax documents early to avoid any last-minute surprises.

The shift from EFC to SAI

For years, the FAFSA calculated the Expected Family Contribution (EFC), an estimate of how much a family could reasonably contribute to college costs. This number was often misunderstood and caused confusion. The 2026-2027 FAFSA replaces the EFC with the Student Aid Index (SAI). While both numbers serve a similar purpose – determining financial need – the calculation is different.

The SAI calculation takes into account family size and income, but it doesn’t consider things like home equity or retirement savings. This is a significant change. Previously, home equity was a factor in determining the EFC, which could have reduced aid eligibility for families with substantial homeownership. The SAI is intended to be a more accurate reflection of a family’s ability to pay for college, focusing primarily on current income.

The SAI ranges from -$1,500 to $6,900. A negative number means you have high financial need and likely qualify for the maximum Pell Grant. Just keep in mind that while the federal government uses this number, individual private colleges often use their own separate formulas to decide how much of their own money to give you.

What does your SAI actually mean? It's not the amount your family is expected to pay, but rather a number colleges use to determine how much financial aid you might receive. A lower SAI generally translates to more aid, while a higher SAI means less. Understanding this distinction is key to navigating the financial aid process.

Who gets more aid under the new rules?

The changes to the FAFSA are expected to benefit many low-income students and students from larger families. By excluding home equity and retirement savings from the SAI calculation, these students may be eligible for more Pell Grants and other forms of financial aid. The simplification of the form should also make it easier for these students to apply for aid.

However, not all students will benefit from these changes. Some students with significant assets, particularly those who previously benefited from the home equity exclusion in the EFC calculation, may see a reduction in their aid eligibility. It’s also possible that some middle-income families could see a slight decrease in aid, depending on their specific financial circumstances. These are complexities that families need to be aware of.

Students whose parents are self-employed may face unique challenges. As mentioned earlier, the IRS data exchange may not accurately reflect their income, potentially leading to delays or requiring additional documentation. It's crucial for these students to be prepared to provide detailed financial information. They may want to consult with a tax professional to ensure accuracy.

The Department of Education estimates that approximately 600,000 more students from low-income backgrounds will be eligible for Pell Grants as a result of these changes. While this is a positive development, it’s important to remember that financial aid is often limited, and not all eligible students will receive the full amount they need. It's essential to explore all available funding options, including scholarships and private loans.

EFC vs. SAI: A Comparison of Key Factors

| Family Income | Family Size | Assets | EFC Calculation | SAI Calculation | Potential Aid Impact |

|---|---|---|---|---|---|

| Lower Income | Small (1-2 members) | Minimal | EFC generally lower, reflecting income and size. | SAI may be similar, but considers income more heavily. | Potentially No Change or Slight Decrease in aid. |

| Lower Income | Large (5+ members) | Minimal | EFC significantly lower due to size. | SAI may be less affected by family size, potentially increasing. | Potentially Decrease in aid. |

| Higher Income | Small (1-2 members) | Significant | EFC higher, reflecting income and assets. | SAI will likely be higher, with assets playing a role. | Potentially No Change or Slight Increase in aid. |

| Higher Income | Large (5+ members) | Significant | EFC higher, but partially offset by family size. | SAI may be less affected by family size, potentially increasing. | Potentially Increase in aid. |

| Moderate Income | Moderate Size (3-4 members) | Moderate | EFC calculated considering all factors. | SAI calculation will focus on income, with some consideration for assets. | Potentially No Change. |

| Low Income | Any Size | Substantial | EFC may be low, but assets could increase it. | SAI will likely be lower, with less weight given to assets. | Potentially Increase in aid. |

| Variable Income | Any Size | Minimal | EFC calculation relies on reported income, which can be complex. | SAI will use adjusted gross income (AGI) and may be more streamlined. | Potentially No Change or Slight Increase in aid. |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

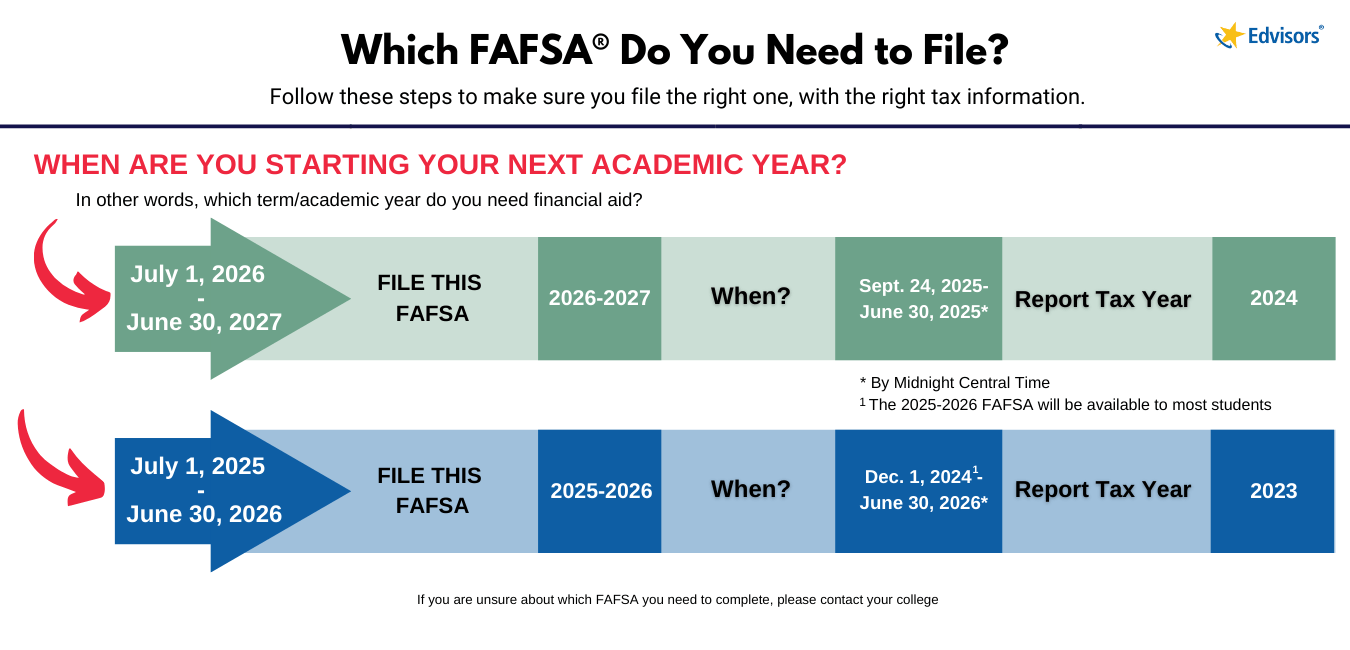

Deadlines you can't miss

The federal FAFSA deadline for the 2026-2027 academic year is typically June 30th. However, this is not a hard and fast rule. Many states and colleges have earlier deadlines, and it's crucial to be aware of these. Applying early is always the best strategy, as some aid is awarded on a first-come, first-served basis.

State deadlines vary significantly. Some states have deadlines as early as February or March. Missing a state deadline could mean missing out on state-funded grants and scholarships. It’s essential to check with your state’s higher education agency to determine the specific deadline. You can find a list of state deadlines on the Federal Student Aid website.

Colleges and universities also have their own FAFSA deadlines. These deadlines are often earlier than the federal or state deadlines. Check with the financial aid office of each school you’re applying to in order to ensure you submit your FAFSA on time. Procrastinating can significantly reduce your chances of receiving aid.

Don't wait until the last minute to complete the FAFSA. Technical issues and unexpected delays can occur. Submitting your application well before the deadline gives you time to resolve any problems and ensures that your application is processed in a timely manner. Prioritize completing the FAFSA as early as possible.

Navigating Dependency Status

Dependency status is a critical factor in determining FAFSA eligibility. Generally, students are considered dependent if they are under the age of 24, unmarried, and do not have dependent children of their own. Dependent students are required to provide their parents’ financial information on the FAFSA.

However, there are exceptions to this rule. Students can be considered independent if they meet certain criteria, such as being married, having children who receive more than half of their support, being a veteran, or having been legally emancipated. Documentation is typically required to verify these circumstances.

There have been some changes to dependency overrides for specific situations. The Department of Education has expanded the definition of “independent student” to include students who are experiencing homelessness or are at risk of homelessness. This is a positive step towards providing aid to students who may be facing challenging circumstances.

A common misconception is that simply living on your own makes you an independent student. This is not true. You must meet one of the specific criteria outlined by the Department of Education to be considered independent. Carefully review the dependency status guidelines on the Federal Student Aid website to determine your eligibility.

Common FAFSA Mistakes and How to Avoid Them

One of the most common FAFSA mistakes is reporting incorrect income information. This can happen if you misread your tax return or if you use outdated information. Always double-check your income figures against your tax documents. Utilizing the IRS data retrieval tool can help minimize this error.

Misreporting assets is another frequent error. Students sometimes forget to include certain assets, such as savings accounts or investments. Be sure to include all of your assets, as well as those of your parents if you are a dependent student. Remember that the SAI does not include home equity, but other assets still need to be reported.

Failing to meet deadlines is a surefire way to miss out on financial aid. As discussed earlier, state and college deadlines can be earlier than the federal deadline. Mark these deadlines on your calendar and submit your FAFSA well in advance.

What if you make a mistake after submitting your FAFSA? You can correct errors online through the FAFSA website. It’s important to make corrections as soon as possible to avoid delays in processing your aid. Keep a record of all changes you make.

Resources for FAFSA Help

The Federal Student Aid website () is the primary resource for FAFSA information. The website offers a wealth of information, including detailed instructions, FAQs, and tutorials. It’s a great place to start if you have questions about the FAFSA.

Your college’s financial aid office is another valuable resource. Financial aid counselors can provide personalized assistance and answer your specific questions. Don’t hesitate to reach out to them for help. They are there to support you through the financial aid process.

Several non-profit organizations offer free FAFSA assistance. These organizations can provide guidance and support to students and families who need help completing the FAFSA. Some examples include Sallie Mae and local community organizations focused on education access.

If the online help tools fail, call your target school's financial aid office directly. They usually have the most up-to-date information on how the new federal changes affect their specific campus aid packages.

Helpful Resources

- Federal Student Aid - The official website for FAFSA, providing updates on changes, application instructions, and student aid information.

- College Board - Offers resources to help students plan and pay for college, including information on FAFSA and financial aid.

- Sallie Mae - Provides information and tools related to saving, planning, and paying for college, including resources on understanding the FAFSA.

- Khan Academy - Offers free educational resources, including a dedicated section on navigating the FAFSA process with instructional videos and practice exercises.

- Federal Student Aid Information Center (FSAIC) - Contact the FSAIC directly with questions about the FAFSA or federal student aid programs.

- Your High School Counseling Office - Counselors can provide personalized guidance on completing the FAFSA and understanding your financial aid options.

- Local Non-Profit Organizations - Many community organizations offer free FAFSA assistance workshops and one-on-one counseling. Search online for organizations in your area.

No comments yet. Be the first to share your thoughts!