The FAFSA is Changing: Here's What You Need to Know

The Free Application for Federal Student Aid (FAFSA) is undergoing a major overhaul for the 2026-2027 academic year. This isn’t a minor update; it’s a fundamental redesign aimed at simplifying the process, expanding eligibility for aid, and ultimately improving student outcomes. The Department of Education has been working to make college more accessible by reducing barriers to financial aid.

These changes come after a rocky rollout of the updated FAFSA for the 2024-2025 school year, which experienced significant delays and technical issues. Those challenges have informed the planning for the 2026-2027 version, with a greater emphasis on thorough testing and a smoother implementation. The goal is to avoid repeating those past mistakes.

The core idea behind the FAFSA simplification is to make applying for aid less daunting. For years, students and families have struggled with a lengthy and complex form. The new FAFSA strives to be more user-friendly, reducing the time and effort required to complete it. It's a significant shift in how federal student aid is determined and distributed.

Ultimately, the Department of Education hopes these changes will encourage more students, particularly those from low-income backgrounds, to pursue higher education. They believe that removing obstacles in the financial aid process will lead to increased college enrollment and completion rates. This is a really positive development for students across the country.

A Simplified Application: What’s Different?

One of the most noticeable changes is a significant reduction in the number of questions asked on the FAFSA. The new form is expected to be considerably shorter and more streamlined than its predecessor. This simplification is designed to make the application process less overwhelming for students and families.

The language used in the FAFSA is also being revised to be clearer and more accessible. Jargon and confusing terminology are being replaced with plain language, making it easier for everyone to understand what information is being requested. This is a welcome change for many who found the old FAFSA needlessly complicated.

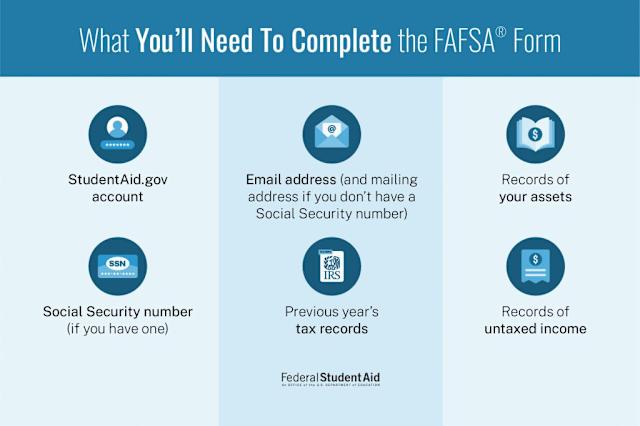

A major improvement is the direct data import from the IRS. This allows students and parents to securely transfer their tax information directly into the FAFSA, eliminating the need to manually enter data from tax returns. This feature will dramatically reduce errors and save time. It’s a big step toward accuracy.

Several questions that were previously asked on the FAFSA have been removed. These include questions about parental drug convictions and selective service registration. The Department of Education determined these questions were unnecessary and potentially discouraged eligible students from applying. This change is about removing barriers to access.

Perhaps the biggest conceptual change is the replacement of the Expected Family Contribution (EFC) with the Student Aid Index (SAI). The EFC was often misunderstood and didn’t accurately reflect a family’s ability to pay for college. The SAI aims to be a more accurate and equitable measure of financial need.

- Reduced number of questions

- Simplified language

- Direct IRS data import

- Removal of unnecessary questions

- Replacement of EFC with SAI

Understanding the Student Aid Index (SAI)

The Student Aid Index (SAI) is the new metric used to determine how much a student and their family can reasonably contribute to the cost of college. It replaces the Expected Family Contribution (EFC), and the goal is to provide a more accurate picture of a family’s financial situation. However, it’s still a complex calculation, and understanding it is crucial for maximizing aid eligibility.

The SAI calculation differs from the EFC in several key ways. The EFC considered a wider range of assets and income sources, and it often penalized families for saving for retirement or owning a small business. The SAI places less emphasis on these factors, focusing more on current income and family size.

Family income and size are the primary factors influencing the SAI. However, the weighting of these factors is complex. The SAI calculation includes an income protection allowance, which shields a portion of a family’s income from being considered in the calculation. The size of this allowance varies depending on family size and income level.

Currently, the exact formulas used to calculate the SAI are still being finalized and clarified by the Department of Education. However, it’s generally understood that the SAI will be more favorable to low-income families than the EFC was. Families with incomes below a certain threshold may have a SAI of zero, making them eligible for the maximum amount of Pell Grant funding.

It’s important to note that the SAI is not the amount a family is expected to pay out of pocket. It’s simply an index number used by colleges and universities to determine a student’s financial need. Each school then uses its own methodology to calculate a student’s financial aid package, taking into account the SAI and other factors.

Income Reporting: Direct Data Exchange

The direct data exchange with the IRS is a game-changer for the FAFSA. Using the IRS Data Retrieval Tool (DRT) allows students and parents to securely transfer their tax information directly into the FAFSA form with a few simple clicks. This eliminates the need to manually enter tax data, reducing errors and saving considerable time.

The benefits of using the DRT are significant. It improves accuracy, speeds up the application process, and reduces the risk of identity theft. The tool retrieves information such as adjusted gross income (AGI), tax filing status, and tax liability directly from the IRS database.

However, there are potential issues students might encounter. Some students or parents may not have access to the IRS data, for example, if they haven’t filed taxes or if they filed a paper return. In these cases, alternative verification methods will be available, but they may require additional documentation.

Privacy concerns surrounding the direct data exchange are understandable. The Department of Education has taken steps to ensure the security of this data transfer, including using encryption and implementing strict access controls. Students and parents can be confident that their tax information is being protected.

- Securely transfers tax information

- Improves accuracy

- Speeds up the process

- Reduces risk of identity theft

Divorce, Separation, and Remarriage: New Rules

The FAFSA changes significantly affect how divorced or separated parents’ income is handled. Under the new rules, the parent with whom the student lived the most during the past 12 months will generally be the parent whose income is reported on the FAFSA. This is a shift from the previous rule, which often required income information from both parents.

If the student did not live with either parent during the past 12 months, the income of the parent who provided the most financial support will be reported. Documentation may be required to verify living arrangements and financial support. This is a point where students might need to gather supporting documents.

Situations involving remarriage and stepparent income also have new rules. If the custodial parent has remarried, the income of the stepparent will be included on the FAFSA. This is because the stepparent’s income is considered to be available to support the student.

These changes are designed to simplify the process and ensure that the FAFSA accurately reflects a student’s financial situation. It’s important for students with divorced or separated parents to carefully review the FAFSA instructions and gather any necessary documentation.

Impact on Different Student Profiles

The FAFSA changes will have a varying impact on different types of students. Low-income students are likely to benefit the most, as the SAI is designed to be more favorable to families with limited financial resources. The increased income protection allowance will shield more of their income from being considered in the calculation.

Students from single-parent households may also see an increase in aid eligibility, particularly if the custodial parent has a low income. The simplification of the FAFSA and the removal of questions about parental drug convictions could also encourage more students from these households to apply for aid.

Students with large families will benefit from the SAI’s consideration of family size. The income protection allowance increases with family size, meaning that a larger portion of their income will be protected from being considered in the calculation. This could result in a lower SAI and increased aid eligibility.

Students with significant assets may see a smaller impact from the FAFSA changes. While the SAI places less emphasis on assets than the EFC, assets are still considered to some extent. However, the overall impact is likely to be less significant for students with substantial savings or investments.

Potential Impact of FAFSA Changes (2026-2027) on Different Student Profiles

| Student Profile | SAI Calculation Impact | Asset Reporting Impact | Parental Income Consideration | Overall Aid Eligibility |

|---|---|---|---|---|

| Low-income, Single-Parent Household | Likely to see a more accurate SAI reflecting income, potentially increasing aid. | Asset reporting simplification may have minimal impact as assets are likely limited. | Parental income will continue to be a primary factor, but the new SAI calculation aims for fairness. | Potentially increased eligibility for Pell Grants and other need-based aid. |

| Middle-income, Two-Parent Household | SAI calculation changes may result in a different aid assessment; impact depends on specific income and asset details. | Simplified asset reporting may reduce documentation burden. | Parental income remains central, but the new formula considers more factors. | Aid eligibility could increase, decrease, or remain the same depending on individual circumstances. |

| High-income, No-Parent Contribution | SAI will likely be significantly higher, potentially reducing eligibility for need-based aid. | Asset reporting simplification is unlikely to substantially alter eligibility. | Parental income is less relevant, but student's income and assets will be heavily considered. | Reduced eligibility for need-based aid; may need to rely more on loans or savings. |

| High-income, Large Family | The revised SAI calculation may offer some benefit due to the consideration of family size, but high income will still be a major factor. | Simplified asset reporting may be helpful, but unlikely to offset high income impact. | Parental income will be a significant factor, but the new formula may provide some adjustment for larger families. | Aid eligibility may be limited, but potentially more favorable than under the previous system. |

| Independent Student, Low Income | Likely to see a more accurate SAI reflecting income, potentially increasing aid. | Asset reporting simplification may be beneficial. | Student income is the primary factor; parental income is not considered. | Potentially increased eligibility for need-based aid. |

| Independent Student, Moderate Income | SAI calculation changes may result in a different aid assessment; impact depends on specific income and asset details. | Simplified asset reporting may reduce documentation burden. | Student income is the primary factor. | Aid eligibility could increase, decrease, or remain the same depending on individual circumstances. |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

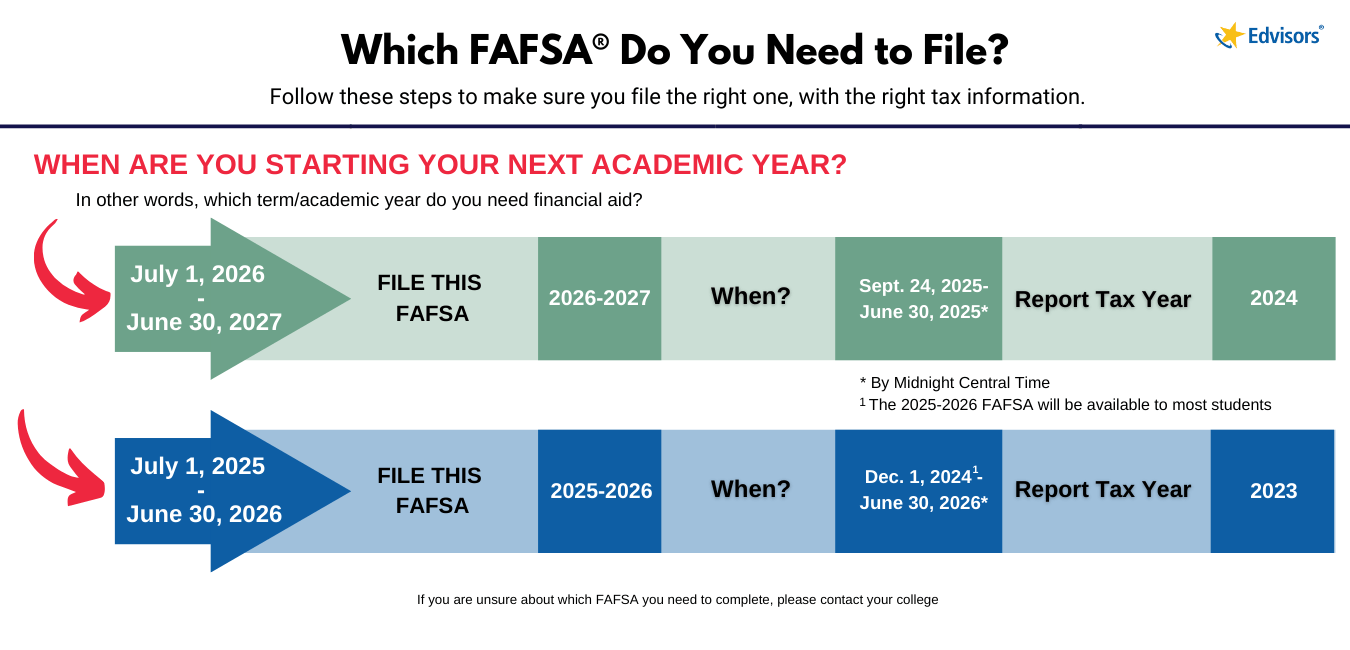

FAFSA Deadlines and Important Dates

The federal FAFSA deadline is typically June 30th of each year, but it’s crucial to submit the FAFSA as early as possible. Many states and colleges have their own deadlines, which may be much earlier than the federal deadline. Missing these deadlines could mean missing out on financial aid.

Submitting the FAFSA early is especially important for students who are eligible for need-based aid, such as Pell Grants. These funds are limited, and they are awarded on a first-come, first-served basis. The earlier you apply, the better your chances of receiving aid.

If a student misses the FAFSA deadline, they may still be able to submit a late application. However, their eligibility for aid may be limited, and they may not receive as much funding as they would have if they had applied on time. It's always best to avoid this situation by submitting the FAFSA well before the deadline.

Resources and Where to Get Help

Navigating the FAFSA can be challenging, but there are many resources available to help students and families. The Federal Student Aid website () is the official source of information about federal student aid programs.

State financial aid agencies also offer valuable resources, including information about state-specific grants and scholarships. You can find a list of state agencies on the Federal Student Aid website. College financial aid offices are another great resource. They can provide personalized guidance and answer your questions about the FAFSA and financial aid options.

Several non-profit organizations offer free financial aid counseling. These organizations can help you understand the FAFSA, complete the application, and explore different financing options. Don't hesitate to reach out for help if you need it.

- Federal Student Aid:

- State Financial Aid Agencies: Available through the Federal Student Aid website

- College Financial Aid Offices

- Non-profit Financial Aid Counseling Organizations

No comments yet. Be the first to share your thoughts!