The FAFSA is Changing: What Students and Families Need to Know for 2026-2027

The Free Application for Federal Student Aid, or FAFSA, is undergoing significant changes for the 2026-2027 school year. These aren't just minor adjustments; it’s a complete overhaul of the form and the underlying methodology for determining financial aid eligibility. The Department of Education aims to simplify the process and expand access to aid, but the rollout has been… bumpy, to say the least. The Department of Education is still releasing technical specifications for the new cycle.

The driving force behind these changes is the FAFSA Simplification Act, passed in 2020. The goal is to make the FAFSA easier to complete, increasing the number of students – particularly those from low-income backgrounds – who apply for and receive financial aid. A major component is a shift away from using the Expected Family Contribution (EFC) and toward the Student Aid Index (SAI).

Right now, a lot of details are still being finalized and implemented. It’s a bit chaotic, and information is evolving rapidly. I’m focusing on what’s confirmed by the Department of Education as of today, acknowledging that things could shift. Stay tuned to the Federal Student Aid website for the latest updates.

These changes impact everyone applying for federal financial aid, from first-time freshmen to returning students. Missing these updates can cost you thousands in aid. Check your specific state and college deadlines, as they often fall months before the federal cutoff.

Understanding the New FAFSA Simplification Act Changes

The FAFSA Simplification Act overhaul is now in effect. Perhaps the most significant is the elimination of the Expected Family Contribution (EFC). For years, the EFC was a number used to estimate how much a family could contribute toward college costs. It’s now being replaced with the Student Aid Index (SAI).

The SAI is calculated using a slightly different formula and considers a smaller number of assets than the EFC did. Critically, the SAI won’t include assets in 529 plans for the student or parent. This is a big win for families who have been diligently saving for college. However, it’s not a simple swap; the SAI is not a direct 1:1 replacement for the EFC.

Another major change involves how income is reported. Previously, students and families had to manually enter income information from their tax returns. Now, the FAFSA will directly import income data from the IRS, using a process called direct data exchange. This should significantly reduce the amount of manual data entry required. Although, there are potential issues that we’ll address later.

The SAI calculation also features changes to income protection allowances. These allowances shield a portion of a family’s income from being considered when determining aid eligibility. The income protection allowance is based on family size and adjusted gross income (AGI). The higher your AGI, the smaller the allowance.

- Elimination of EFC: Replaced with the Student Aid Index (SAI).

- Direct Data Exchange: Income data automatically imported from the IRS.

- Simplified Income Reporting: Fewer questions about income and assets.

- Increased Income Protection Allowance: More income shielded from calculation.

EFC vs. SAI: A Comparison of Calculation Factors

| Calculation Factor | EFC (Expected Family Contribution) | SAI (Student Aid Index) | Impact on Aid Eligibility |

|---|---|---|---|

| Income | Assessed at a fixed percentage, with diminishing returns as income rises. Higher income generally leads to a higher EFC. | Considers Adjusted Gross Income (AGI) and allows for a simplified income calculation for many families. Income protection allowances are more generous, potentially lowering the SAI for lower-income families. | A lower SAI, resulting from more generous income allowances, typically increases aid eligibility. The shift aims to protect a larger portion of a family’s income. |

| Assets | Included home equity, savings, and investments. A percentage of assets were considered available for educational expenses. | Excludes assets for families with less than $50,000 in assets. For families with assets above this threshold, a smaller percentage is assessed compared to EFC. | The reduced weighting of assets under SAI, and the asset protection threshold, generally increases aid eligibility, particularly for families with modest savings. |

| Family Size | Adjusted the income and asset contribution expectations based on the number of people in the household. Larger families had a lower EFC. | Similar to EFC, family size continues to be a significant factor, adjusting the SAI based on the number of individuals supported by the family’s income and resources. | The impact of family size remains consistent – larger families generally qualify for more aid due to a lower SAI. |

| Weighting of Factors | Income and assets were weighted relatively equally, with a formula determining the contribution amount. | SAI places a greater emphasis on income as the primary factor, with assets playing a less significant role, especially for families with limited resources. | The shift in weighting prioritizes families’ current income, aiming to provide more equitable access to aid based on immediate financial circumstances. |

| Complexity | Calculation could be complex, requiring detailed financial information and potentially leading to errors. | Designed to be simpler, particularly with the introduction of direct data exchange with the IRS for many filers, reducing the need for manual input. | Simplified calculation reduces errors and increases accessibility, potentially leading to more accurate aid awards. |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Who Benefits (and Doesn't) from the New FAFSA?

While the FAFSA Simplification Act aims to benefit all students, the reality is that the impact will be uneven. Lower-income students are expected to be the biggest winners. The changes to the SAI calculation, particularly the increased income protection allowance, will likely result in a higher SAI for these students, leading to increased financial aid eligibility.

Students from families with complex financial situations – such as those with multiple jobs, self-employment income, or significant medical expenses – may also benefit. The simplification of the form could reduce the burden of reporting these complex financial details. However, it’s not a guarantee.

Families with significant assets may see little to no change, or even a decrease in aid. While 529 plans are no longer considered in the SAI calculation, other assets – such as savings accounts, investments, and real estate – still are. The impact will depend on the specific financial circumstances of each family.

The Brookings Institution and other policy groups are still modeling the full impact. Early data indicates middle-income families may see small aid increases, while high-asset households could see their eligibility drop.

Will the New FAFSA Benefit You?

The 2026-2027 FAFSA introduces significant changes designed to simplify the application process and expand financial aid eligibility. This short quiz will help you get a general idea of whether these changes might increase your potential aid. Keep in mind this is a quick assessment and doesn’t guarantee specific outcomes.

Navigating the New Income Reporting Requirements

The shift to direct data exchange with the IRS is a monumental change. The FAFSA will now automatically pull income information from the IRS, streamlining the application process. This means students and families will need to provide their Federal Student Aid ID (FSA ID) and consent to allow the IRS to share their tax information.

However, it’s not a completely hands-off process. Students and families will still need to provide some information manually, such as their Social Security numbers, date of birth, and marital status. They’ll also need to indicate whether they filed taxes and which tax year they’re reporting.

There are potential concerns about data privacy and security with this new system. The Department of Education has assured the public that robust security measures are in place to protect sensitive tax information, but it’s understandable to be wary. If you’re uncomfortable with sharing your tax information directly, you may be able to manually enter your income information, but this is a more time-consuming process.

If there are discrepancies between the information reported to the IRS and the information on the FAFSA, the Department of Education will likely flag your application for verification. This could delay the processing of your aid. It’s crucial to ensure that the information you provide on the FAFSA is accurate and consistent with your tax return.

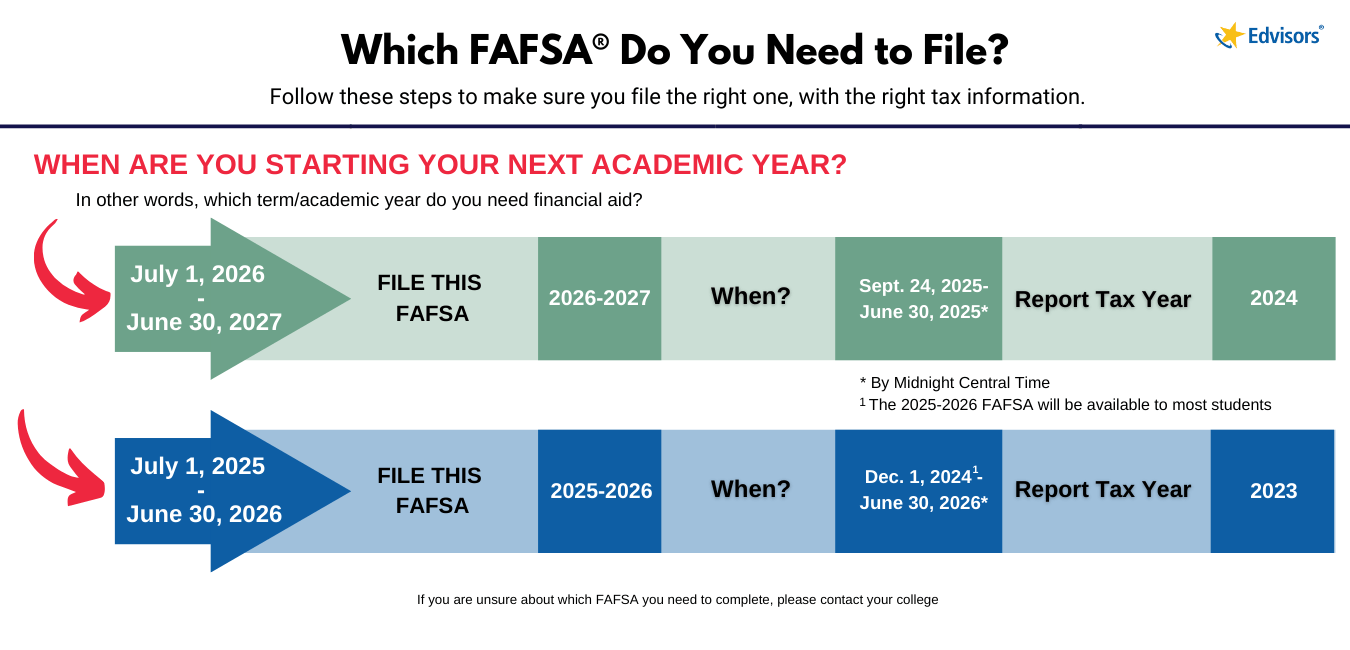

Important Dates and Deadlines for the 2026-2027 FAFSA

Currently, the FAFSA is scheduled to open on October 1st, 2025, for the 2026-2027 academic year. However, this date is always subject to change, especially given the ongoing implementation of the FAFSA Simplification Act. Keep a close eye on the Federal Student Aid website for updates.

State aid deadlines vary significantly. Many states have priority deadlines – meaning that students who submit the FAFSA by a certain date will receive priority consideration for state grants and scholarships. These deadlines can be as early as November or December. Check with your state’s higher education agency for specific deadlines.

The federal deadline for submitting the FAFSA is generally June 30th of the award year. However, it’s crucial to submit the FAFSA as early as possible, even if the direct data exchange with the IRS isn’t fully functional. This will give you the best chance of receiving the maximum amount of aid.

If you miss a deadline, don’t panic. You may still be able to submit the FAFSA and receive some financial aid, but your options may be limited. It’s always better to submit on time, if possible.

Troubleshooting Common FAFSA Issues and Where to Get Help

The FAFSA can be a source of frustration for many students and families. Common issues include incorrect information, difficulties with data retrieval from the IRS, and confusion about the SAI calculation. If you encounter any problems, don’t hesitate to seek help.

The Federal Student Aid Information Center (FSAIC) is your primary resource for assistance. You can reach them by phone at 1-800-4-FED-AID (1-800-433-3243) or online through their website. Be prepared for potentially long wait times, especially during peak periods.

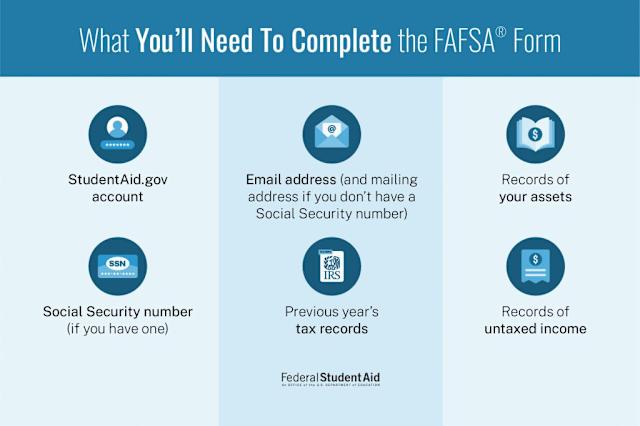

Visit StudentAid.gov to create your FSA ID before the October 1st opening date. official website of the Department of Education and provides comprehensive guidance on the FAFSA. Many colleges and universities also have financial aid offices that can provide personalized assistance.

A great tip is to carefully review your completed FAFSA submission summary before submitting. This summary provides a snapshot of the information you’ve entered and can help you identify any errors or inconsistencies. Don't be afraid to double-check everything!

Understanding Dependency Status and Special Circumstances

Dependency status is a critical factor in determining financial aid eligibility. Students are generally considered dependent if they are under the age of 24, unmarried, and do not have dependents of their own. Dependent students are required to provide their parents’ income information on the FAFSA.

However, there are exceptions to these rules. Students who meet certain criteria – such as being married, having children, being a veteran, or being an orphan – may be considered independent. If you’re unsure about your dependency status, consult the FAFSA handbook or contact the Federal Student Aid Information Center.

If you have special circumstances – such as parental separation, loss of income, or significant medical expenses – that aren’t accurately reflected in the standard FAFSA form, you can submit a professional judgment appeal. This appeal asks the financial aid office to review your case and make adjustments to your aid package.

The process for submitting a professional judgment appeal varies by college. You’ll typically need to provide documentation to support your claim, such as divorce decrees, medical bills, or letters from employers. It can be a bit daunting, but it’s worth it if your situation warrants a review.

Resources for Finding Scholarships and Grants

The FAFSA is just the first step in funding your education. Don’t underestimate the power of scholarships and grants. These sources of funding don’t need to be repaid, making them an invaluable resource.

Several online scholarship search engines can help you find opportunities that match your qualifications. Some popular options include Scholarships.com, Fastweb, and Sallie Mae’s Scholarship Search. Be sure to read the eligibility requirements carefully before applying.

Your state’s higher education agency may also offer grant programs. These grants are typically need-based and can provide significant financial assistance. Check your state’s website for more information.

Don't forget to explore scholarships offered by your college or university. Many institutions have their own scholarship programs that are specifically designed for their students. A well-crafted essay can make all the difference.

DOGE is considering replacing human call center workers with AI to handle student loan questions. 1,600 jobs on the line. pic.twitter.com/7kjwbIOs41

— Grace Chong, MBI (@gc22gc) February 13, 2025

No comments yet. Be the first to share your thoughts!