Federal vs. Private: The Core Differences

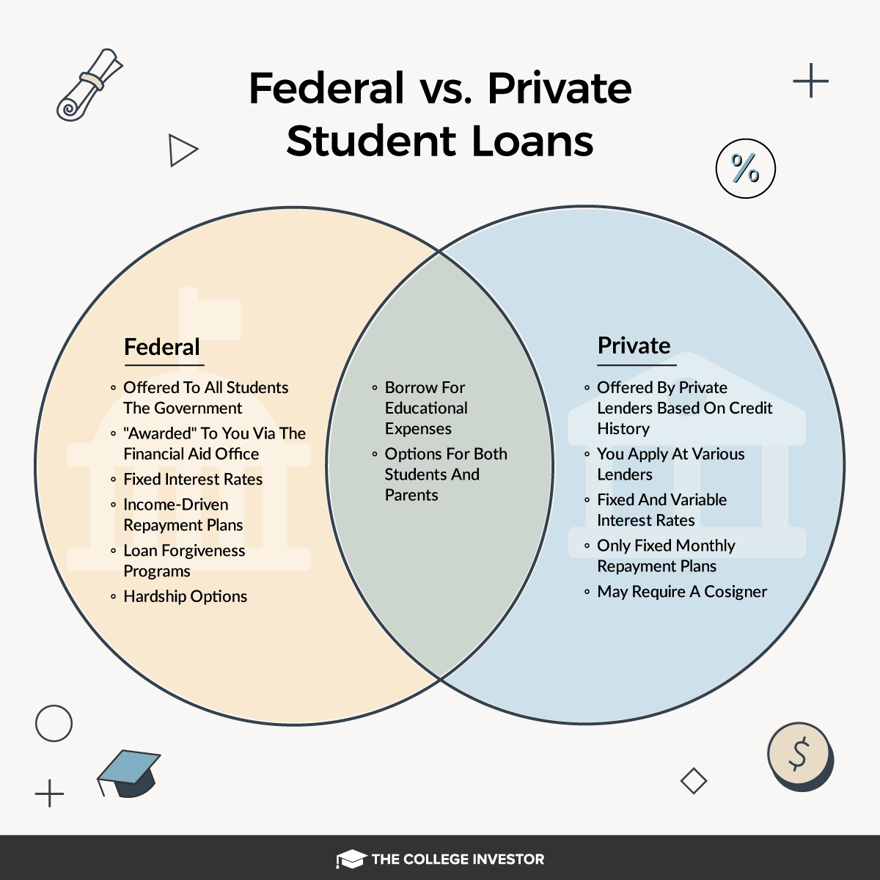

Understanding student loans can feel overwhelming, but the first step is grasping the fundamental difference between federal and private options. Federal student loans are issued by the U.S. Department of Education and come with specific protections and repayment plans. They’re designed to be more accessible, often requiring no credit check. Private student loans, on the other hand, are offered by banks, credit unions, and other private lenders.

The biggest distinction is who backs these loans. Federal loans have the full backing of the government, which provides certain benefits like fixed interest rates and flexible repayment options. Private loans don’t have this backing, meaning they rely on your creditworthiness for approval and typically have fewer built-in protections. Eligibility for federal loans is primarily based on financial need, as determined by the FAFSA.

Loan limits also differ significantly. Federal loans have annual and aggregate limits that vary depending on your year in school and dependency status. Private loans generally allow you to borrow up to the cost of attendance, minus any other financial aid you receive, but this is heavily dependent on your credit history. Federal loans are the best starting point because they offer protections private lenders won't match.

The application process is another key difference. Federal loans require completing the Free Application for Federal Student Aid (FAFSA), a standardized form used to assess your financial need. Private loans require a separate application with each lender, and often involve a credit check and documentation of income. I always recommend exhausting federal options before considering private loans.

Interest rates for 2026

Interest rates dictate your long-term costs. Congress sets federal rates annually, and once you borrow, that rate is fixed. For the 2025-2026 academic year, undergraduate Direct loans sit at 5.05%, while graduate loans reach 6.82% and PLUS loans hit 8.08%.

Specifically, on March 10, 2026, a court order ended the Saving on a Valuable Education (SAVE) Plan. The U.S. Department of Education will be contacting impacted borrowers, and they can explore and apply for other repayment plans. You can find more information at StudentAid.gov/courtactions. This change highlights the potential for federal loan terms to shift, making it even more important to stay informed.

Private loan interest rates are a different story. They’re determined by the lender based on your credit score, income, loan term, and the overall economic climate. In 2026, with interest rates expected to remain relatively stable, borrowers with excellent credit could potentially find rates starting around 6%, while those with fair credit might face rates closer to 12% or higher. These are estimates, of course.

A crucial point is that many private loans offer variable interest rates, meaning the rate can change over the life of the loan based on market fluctuations. This can be beneficial if rates fall, but it also carries the risk of your payments increasing. Fixed-rate private loans are also available, offering more predictability but often at a slightly higher initial rate. For example, Sallie Mae currently offers variable rates starting at 7.74% and fixed rates starting at 8.24% (as of November 2023 – rates are subject to change).

Here's a quick comparison as of late 2023: | Loan Type | Rate Type | Estimated Range (2026) | |---|---|---| | Federal Direct Subsidized/Unsubsidized (Undergrad) | Fixed | 5.05% | | Federal Direct Unsubsidized (Graduate) | Fixed | 6.82% | | Federal Direct PLUS | Fixed | 8.08% | | Private (Excellent Credit) | Variable/Fixed | 6% - 13% | | Private (Fair Credit) | Variable/Fixed | 10% - 18% +

Federal vs. Private Loan Interest Rates (2026 Estimates)

| Loan Type | Rate Type | Typical Range (2026) | Factors Influencing Rate |

|---|---|---|---|

| Federal Subsidized Loans | Fixed | 5.50% (estimated - subject to annual adjustments) | Federal law, grade level, and loan disbursement date. |

| Federal Unsubsidized Loans | Fixed | 6.50% (estimated - subject to annual adjustments) | Federal law, grade level, and loan disbursement date. |

| Private Loans (Excellent Credit) | Fixed/Variable | Variable: 6.0% - 12.0%, Fixed: 7.0% - 14.0% | Credit score, income, loan term, lender, and whether the rate is fixed or variable. |

| Private Loans (Average Credit) | Fixed/Variable | Variable: 8.0% - 15.0%, Fixed: 9.0% - 16.0% | Credit score, income, loan term, lender, and whether the rate is fixed or variable. |

| Federal Subsidized Loans | Fixed | Government sets rates annually on July 1st and October 1st. | Set by Congress; generally lower than unsubsidized and private loans. |

| Federal Unsubsidized Loans | Fixed | Government sets rates annually on July 1st and October 1st. | Set by Congress; generally higher than subsidized loans. |

| Private Loans (Excellent Credit) | Variable | Often tied to the Prime Rate or SOFR + a margin. | Market conditions, Prime Rate/SOFR fluctuations, lender’s risk assessment. |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Borrowing limits

Federal student loan limits vary depending on your dependency status (whether you’re claimed as a dependent on your parents’ taxes) and your year in school. For dependent undergraduates, the annual loan limits are $5,500 for first-year students, $6,500 for sophomores, and $7,500 for juniors and seniors. Aggregate (total) limits are $30,000. Independent undergraduates have higher limits: $9,500, $10,500, $12,500, and an aggregate of $57,500.

Graduate students are eligible to borrow up to $20,500 per year, with an aggregate limit of $138,500, including any undergraduate loans. PLUS Loans, available to parents and graduate students, allow borrowing up to the cost of attendance minus other financial aid. These limits are set by the Department of Education and are subject to change, but generally provide a substantial amount of funding.

Private loan limits are much more flexible, but are ultimately determined by the lender and your creditworthiness. Most private lenders will allow you to borrow up to the cost of attendance, but approval isn’t guaranteed. Lenders like SoFi and Earnest will assess your income, credit score, and debt-to-income ratio to determine how much they’re willing to loan you.

If you exhaust your federal loan options and still need funding, private loans become a necessity. However, it's vital to understand that exceeding federal limits often means facing higher interest rates and fewer repayment protections with private loans. It's a trade-off to carefully consider.

Repayment options

Federal student loans offer a variety of repayment plans designed to fit different financial situations. The Standard Repayment Plan is the default, with fixed monthly payments over 10 years. The Graduated Repayment Plan starts with lower payments that increase over time, while the Extended Repayment Plan stretches payments over up to 25 years, potentially lowering monthly amounts but increasing the total interest paid.

Income-Driven Repayment (IDR) plans are particularly popular, as they base your monthly payments on your income and family size. The most talked-about plan, SAVE (Saving on a Valuable Education), has recently undergone changes. As of March 10, 2026, a court order ended the SAVE plan, and the Department of Education will contact affected borrowers. You can find more details and alternative plans at StudentAid.gov/courtactions.

Other IDR plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR). Each plan has its own eligibility requirements and formulas for calculating payments. Some plans also offer loan forgiveness after a certain number of years of qualifying payments. Understanding these differences is crucial for choosing the right plan.

Private student loans, unfortunately, offer far fewer repayment options. Most lenders provide standard repayment terms, typically ranging from 5 to 20 years. Deferment and forbearance options may be available for temporary hardship, but these usually come with continued interest accrual. Loan forgiveness is rarely an option with private loans. Sallie Mae, for instance, offers a limited number of forbearance options, but generally doesn’t offer income-based repayment.

Here's a quick comparison of federal plans: Standard: Fixed payments for 10 years. Graduated: Payments start low and increase over time. Extended: Payments over up to 25 years. SAVE: (Ending March 10, 2026) Income-based, with potential for forgiveness. IBR: Income-based, with potential for forgiveness. PAYE: Income-based, with potential for forgiveness. * ICR: Income-based, with potential for forgiveness.

Federal Repayment Plan Comparison

- Standard Repayment Plan - Fixed payments for up to 10 years; fastest repayment, lowest total interest paid, but highest monthly payments.

- Graduated Repayment Plan - Payments start low and increase every two years, typically over 10 years; good for those expecting income growth, but can lead to higher total interest paid.

- Extended Repayment Plan - Fixed or graduated payments over up to 25 years; lowers monthly payments, but significantly increases total interest paid.

- SAVE (Saving on a Valuable Education) Plan - Income-driven repayment (IDR) plan; payments are based on income and family size, potentially as low as $0; forgiveness after 20-25 years. Unpaid interest may be subsidized by the government.

- Income-Based Repayment (IBR) Plan - IDR plan; payments capped at 10-15% of discretionary income; forgiveness after 20-25 years. Available for eligible loans disbursed before July 1, 2014.

- Pay As You Earn (PAYE) Plan - IDR plan; payments capped at 10% of discretionary income; forgiveness after 20 years. Requires demonstrating partial financial hardship.

- Income-Contingent Repayment (ICR) Plan - IDR plan; payments are based on income, family size, and loan balance; forgiveness after 25 years. Generally, the least favorable IDR plan.

Hardship protections

Life throws curveballs, and sometimes borrowers struggle to make their loan payments. Deferment and forbearance are options for temporarily postponing or reducing payments, but they work differently. Deferment allows you to temporarily stop making payments on federal loans, and in some cases, interest doesn't accrue during deferment (depending on the loan type). Forbearance also temporarily stops or reduces payments, but interest always continues to accrue.

Eligibility for deferment and forbearance varies. Federal deferment options are available for those enrolled in school, experiencing economic hardship, or undergoing certain medical treatments. Forbearance is typically granted for broader reasons, such as financial difficulties or health issues. Private loan deferment and forbearance options are at the lender’s discretion and often have stricter requirements. Don't assume you'll automatically qualify.

Loan discharge is a more permanent solution, but it’s reserved for specific circumstances. Federal loans can be discharged if the borrower dies, becomes totally and permanently disabled, or if the school closes while the borrower is enrolled. Private loans generally have fewer discharge options, typically limited to death or total and permanent disability.

It’s important to understand the implications of deferment and forbearance. While they provide temporary relief, they don’t erase the debt, and the accrued interest can significantly increase the total amount owed. Forbearance, in particular, can be a costly option, especially with private loans where interest continues to accumulate without any potential for capitalization relief.

Fees and Origination Costs: The Hidden Expenses

Don’t underestimate the impact of fees on the total cost of your student loans. Federal Direct Loans come with origination fees, which are a percentage of the loan amount deducted from each disbursement. As of 2023, the origination fee is 1.057% for loans disbursed on or after October 1, 2020, and before October 1, 2024. This means for a $10,000 loan, $105.70 would be deducted upfront.

Private lenders also charge fees, though they vary widely. Some lenders may charge application fees, origination fees, or late payment fees. Prepayment penalties (fees for paying off the loan early) were once common, but they are now less frequent. Be sure to carefully review the terms and conditions of any private loan to understand all associated fees.

These fees can add up significantly over the life of the loan, increasing your overall borrowing costs. It’s crucial to factor them into your calculations when comparing loan options. Even a seemingly small origination fee can translate into hundreds or even thousands of dollars over the repayment period.

Here’s a quick comparison: | Fee Type | Federal Direct Loans | Private Loans | |---|---|---| | Origination Fee | 1.057% (as of 2023) | Varies – may or may not be charged | | Application Fee | None | May be charged | | Late Payment Fee | Varies | Varies | | Prepayment Penalty | None | Increasingly rare, but check terms

Federal vs. Private Student Loan Fee Comparison (2026)

| Fee Type | Federal Direct Loan | Private Loan |

|---|---|---|

| Application Fee | Generally None | Common, can vary widely |

| Origination Fee | Varies by loan type, currently ranges from 1.056% to 4.228% | May be present, varies significantly by lender |

| Late Payment Fee | Generally capped, dependent on loan type | Often higher, and varies by lender |

| Prepayment Penalty | Never Charged | Possible, though becoming less common |

| Deferment/Forbearance Fees | Generally None | May be charged by some lenders |

| Loan Transfer Fees | Not Applicable | May be charged when transferring loans |

Qualitative comparison based on the article research brief. Confirm current product details in the official docs before making implementation choices.

Making the Decision: A Framework

Choosing between federal and private student loans is a significant financial decision. Here’s a framework to help you navigate the process. First, assess your credit score. If you have a limited credit history or a low score, federal loans are likely your best option.

Next, determine how much you need to borrow. If your federal loan limits are sufficient to cover your educational expenses, prioritize those. If you need to borrow more, consider private loans, but be prepared for potentially higher interest rates and fewer protections.

Evaluate your expected future earnings. If you anticipate a stable income, you may be comfortable with a fixed-rate private loan. If your income is uncertain, an income-driven repayment plan with a federal loan might be a better choice.

Finally, consider your risk tolerance and repayment preferences. If you prefer the security of fixed payments and potential loan forgiveness, federal loans are the way to go. If you're comfortable with variable rates and have a strong credit history, private loans might be a viable option. This checklist can help: Credit Score: Excellent, Fair, or Limited? Loan Amount: Covered by Federal Loans or Not? Income Stability: Predictable or Uncertain? Risk Tolerance: High or Low? * Repayment Preference: Fixed or Income-Based?

Essential Reading for Smart Student Loan Decisions

Comprehensive guide to understanding student loan debt · Strategies for effective repayment · Empowers borrowers with knowledge

This book provides essential knowledge for borrowers to navigate and manage their student loan debt effectively.

Covers essential personal finance topics for young adults · Practical advice for real-world financial situations · Aims to build a strong financial foundation

This guide offers practical personal finance advice crucial for young adults managing their money and preparing for the future.

Focuses on strategies to graduate college without debt · Provides actionable skills and planning techniques · Aims to equip students for financial independence

This resource offers valuable strategies and skills for students aiming to graduate college with minimal or no student loan debt.

In-depth exploration of student loan options · Guidance on understanding repayment terms · Tools for financial planning related to student debt

This guide offers a thorough understanding of student loans, aiding borrowers in making informed decisions about their repayment.

Simplified approach to student loan repayment · Clear and concise explanations · Focuses on making the repayment process manageable

This book offers a straightforward and easy-to-understand guide to help individuals manage and repay their student loans.

As an Amazon Associate I earn from qualifying purchases. Prices may vary.

No comments yet. Be the first to share your thoughts!