The state of student debt in 2026

Student loan debt continues to be a significant hurdle for millions of Americans. As of late 2024, the total outstanding federal student loan debt is over $1.7 trillion, and many students struggle to navigate the complex system of repayment options. The financial pressures are real, and the process of securing student loans can feel overwhelming.

Recent changes, like the now-paused Saving on a Valuable Education (SAVE) Plan, demonstrate the ongoing efforts to make repayment more manageable. However, these shifts also add to the confusion. Students need clear, personalized guidance more than ever. That’s where artificial intelligence is starting to play a role, offering a new approach to student loan information and assistance.

The traditional methods of finding and applying for student loans often rely on generalized advice and limited comparison tools. This can lead to students accepting loans that aren’t the best fit for their individual circumstances. AI-powered tools aim to change that, promising a more tailored and efficient experience.

How automated matching actually works

AI-powered loan matching uses algorithms to analyze a student's financial situation and identify potential loan options. It’s not simply a search engine that returns a list of lenders; it's a system designed to understand your specific needs and predict which loans will be most suitable. Think of it as a personalized recommendation engine for securing student loans.

These systems work by collecting data from various sources, including your FAFSA information, credit score (when applicable – some tools focus solely on federal loans), the type of school you’re attending, your intended major, and even your career aspirations. The more data the AI has, the more accurate its recommendations can be.

Importantly, the goal isn't always to find the absolute lowest interest rate. While rate shopping is important, AI aims to find the right loan fit – one that considers your long-term financial health and ability to repay. This means factoring in things like loan terms, fees, and potential income after graduation.

The tech is getting better at moving away from generic advice. Instead of giving every student the same three options, these systems look at what you actually plan to earn after graduation.

- FAFSA data like your family assets and income

- Credit Score: (If applicable) A measure of creditworthiness.

- School Type: Public, private, for-profit.

- Major: Field of study, impacting potential income.

- Career Goals: Projected income and employment prospects.

AI Matching Data Points

- FAFSA Information - Expected Family Contribution (EFC), student dependency status, and reported financial need.

- Credit Score & History - Applicant’s creditworthiness, including credit report data and payment history (or co-signer data).

- School Attributes - Public vs. private institution, in-state vs. out-of-state tuition, and school-specific financial aid policies.

- Field of Study - Major and degree level, as certain fields may qualify for specialized loan programs or higher borrowing limits.

- Career Aspirations - Projected income based on chosen career path, influencing affordability assessments and potential repayment plan options.

- Loan Amount Requested - The total amount of funding needed to cover educational expenses.

- Repayment Timeline Preferences - Desired loan term length (e.g., 10 years, 20 years) and preferred repayment strategy.

Finding more than just a low rate

The most obvious benefit of AI-powered loan matching is the ability to quickly compare rates and terms from multiple lenders. But the advantages go far beyond simple rate shopping. These tools can uncover loan options you might not have found on your own, including lesser-known private lenders or specialized loan programs.

Perhaps even more valuable is the ability to predict affordability. By analyzing your intended major and career goals, AI can estimate your potential income after graduation and assess whether you'll be able to comfortably repay the loan. This is a huge step forward in responsible lending, helping students avoid taking on debt they can’t afford.

AI can also help optimize for long-term financial health. For example, it might recommend a longer loan term with lower monthly payments if it predicts you’ll have a period of lower income after graduation. Or, it might suggest prioritizing federal loans over private loans due to the borrower protections they offer.

I believe it’s important to be realistic. AI isn't a magic bullet. Algorithms are only as good as the data they're fed, and they can't account for every possible scenario. However, they can offer a more holistic and data-driven approach to student loan information than traditional methods.

Current Players and Approaches

The market for AI-driven student loan tools is still relatively new, but several companies are emerging as key players. For example, Sallie Mae offers a tool that helps borrowers compare refinancing options, using algorithms to personalize recommendations based on their credit profile and loan terms.

Another company, Laurel Road, focuses on refinancing and offers a streamlined application process powered by AI. They analyze your financial data to determine your eligibility and potential savings. These platforms often emphasize speed and convenience.

Some platforms, like Credible, take a broader approach, allowing you to compare multiple types of loans – including federal consolidation loans and private refinance loans – all in one place. They aim to provide a comprehensive overview of your options.

It’s critical to understand what each platform actually does. Some are primarily marketing tools for lenders, while others are independent comparison sites. Always read the fine print and understand how the platform is compensated. Don't assume that the "best" loan according to an AI is necessarily the best loan for you.

Reading the fine print

While AI-powered loan matching offers many benefits, it’s important to be aware of the potential drawbacks. Data privacy is a major concern. These tools require access to your personal and financial information, so it’s crucial to choose platforms with robust security measures.

You must also verify the information provided by AI tools. Algorithms can make mistakes, and loan terms can change. Always double-check the details with the lender directly before accepting a loan. Don’t rely solely on the AI’s recommendations.

There’s also the possibility of biased algorithms. If the data used to train the AI is skewed, it could lead to unfair or discriminatory outcomes. This is an area where increased transparency and regulation are needed.

Finally, remember that these tools are not a substitute for financial counseling. If you’re struggling with student loan debt, it’s always best to speak with a qualified financial advisor. They can provide personalized guidance and help you develop a comprehensive repayment plan.

- Review Privacy Policies: Understand how your data is collected and used.

- Verify Loan Terms: Double-check the details with the lender.

- Be Aware of Bias: Recognize that algorithms aren't always neutral.

- Talk to a human financial advisor for a second opinion

Federal Aid First: AI's Role

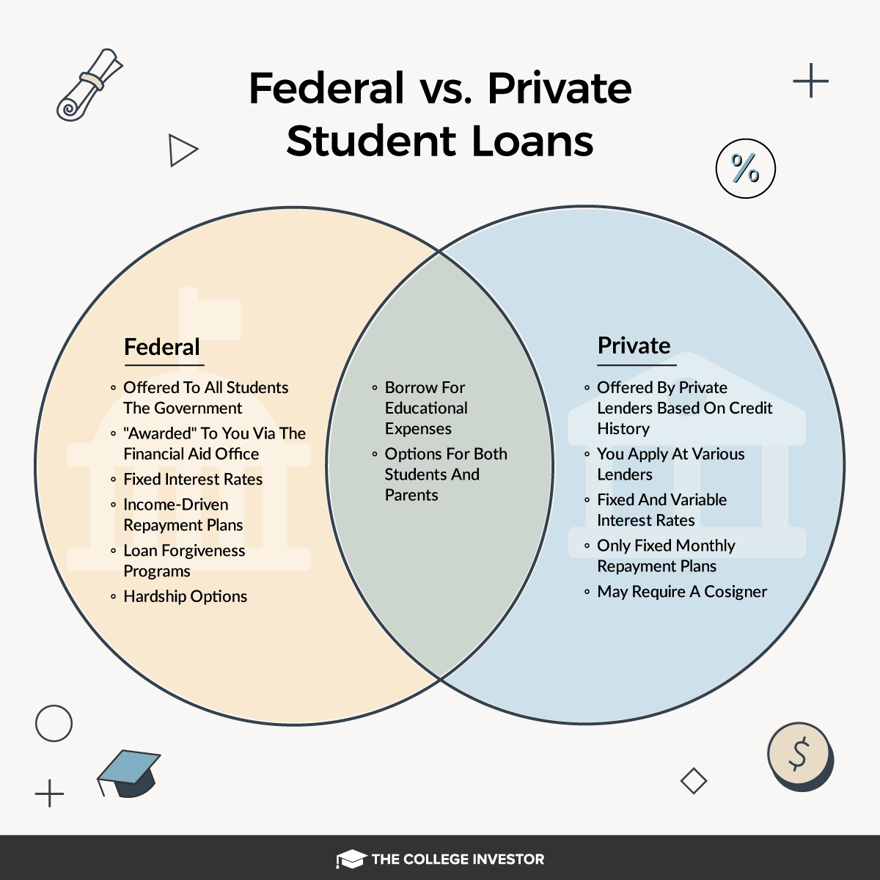

It’s crucial to remember that AI tools should supplement, not replace, the FAFSA process and exploration of federal aid options. Federal student loans generally offer lower interest rates and more flexible repayment plans than private loans. They also come with valuable borrower protections.

AI can actually help you navigate the FAFSA process. Some tools can pre-fill your application based on your financial data, saving you time and reducing the risk of errors. They can also help you understand your eligibility for grants and subsidized loans.

The Department of Education’s website, studentaid.gov, is the best place to start when applying for federal aid. This is your official source for information and applications. AI tools can be a helpful addition, but they should never be used as a substitute for the official government resources.

Before considering private loans, exhaust all federal aid options. AI can assist in this process by clearly outlining your federal aid eligibility and comparing it to potential private loan options. Making informed financial decisions always starts with understanding what federal assistance is available.

No comments yet. Be the first to share your thoughts!