Federal Loan Rates for 2026: A First Look

Federal student loan interest rates for the 2026-2027 academic year are tied to the 10-year Treasury note and set by Congress each spring. Rates are fixed on July 1st, so current numbers are projections based on market conditions.

As of late 2024, rates are expected to remain stable but could change with economic factors. The Department of Education usually announces new rates in May or June. These projections apply to new loans disbursed on or after July 1, 2026.

The three main federal Direct Loans are Subsidized, Unsubsidized, and PLUS Loans. Rates vary by student level (undergraduate, graduate, professional). PLUS Loans, for parents and graduate students, typically have higher rates than undergraduate loans.

Decoding Federal Rate Types

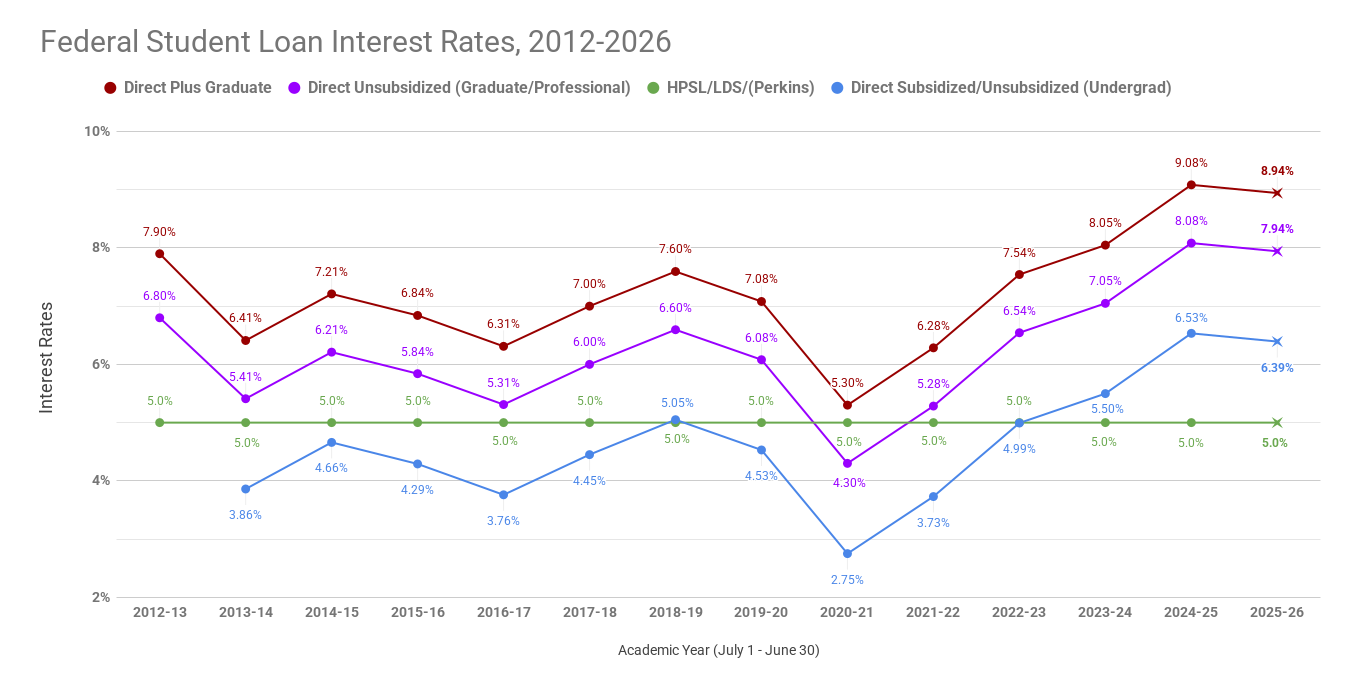

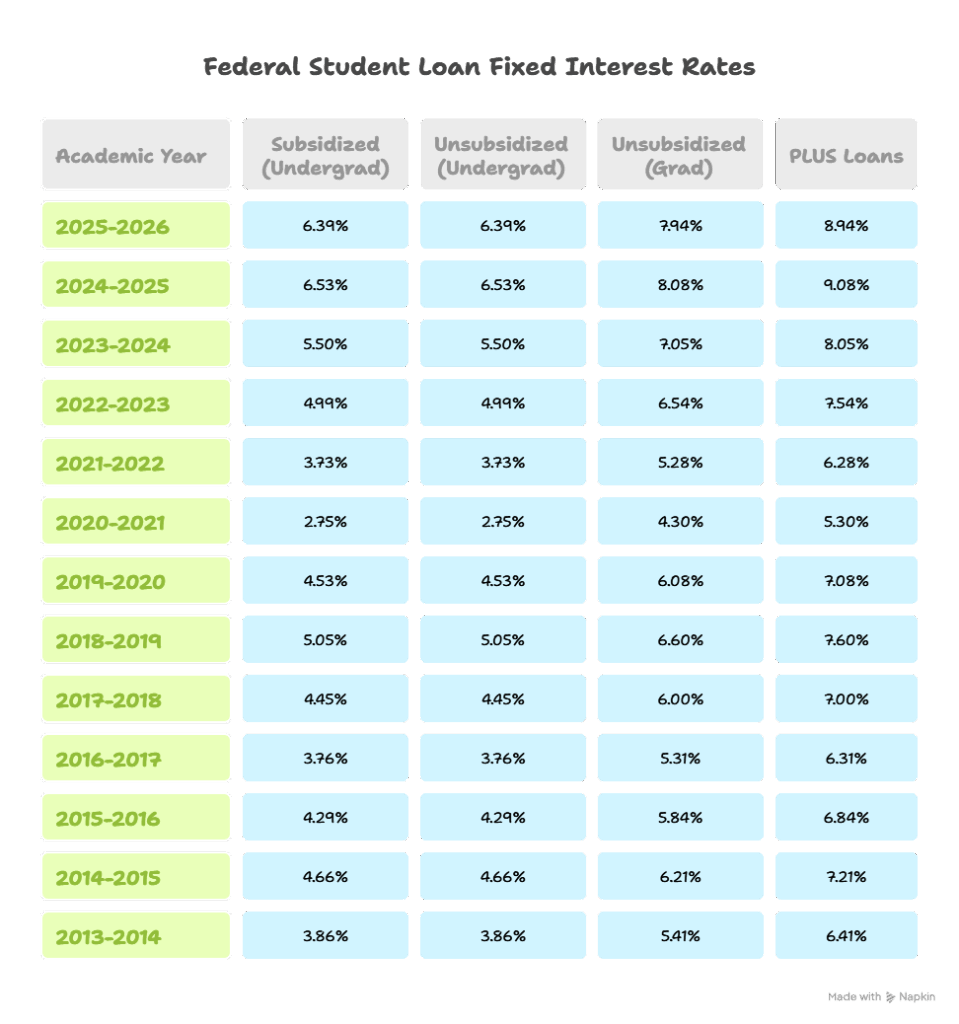

Direct Subsidized Loans are for undergraduates with financial need. The rate (for loans disbursed before July 1, 2024) is 5.05% with a 1.057% loan fee. The government pays interest during school, grace periods, and deferment.

Direct Unsubsidized Loans are for undergraduates and graduates, regardless of need. The current rate is 6.82% with a 1.057% loan fee. Interest accrues from disbursement, increasing the loan balance. Direct PLUS Loans are for parents of dependent undergraduates and for graduate or professional students, with rates at 8.05% and a 4.228% loan fee.

Federal student loans have fixed interest rates, offering predictable repayment. Subsidized loans are more beneficial as interest isn't paid while in school. For example, a $5,000 unsubsidized loan borrowed for four years could accrue hundreds of dollars in interest, increasing the total debt.

- Direct Subsidized Loans: For undergraduates with financial need; government pays interest during deferment.

- Direct Unsubsidized Loans: Available to undergraduates and graduates; interest accrues from disbursement.

- Direct PLUS Loans: For parents and graduate students; generally have the highest rates.

Federal vs. Private Student Loan Comparison (Projected for 2026)

| Loan Type | Eligibility | Interest Rates (Projected) | Loan Limits | Fees & Accrual |

|---|---|---|---|---|

| Direct Subsidized Loan | Undergraduate students with demonstrated financial need | Generally lower; interest may be subsidized while in school | Dependent students: up to $5,500 annually, increasing each year. Independent students: higher limits. | Low fees; interest accrual paused during deferment/grace periods (while in school, for example). |

| Direct Unsubsidized Loan | All undergraduate and graduate students | Generally moderate; interest accrues from disbursement | Dependent students: same as Subsidized. Independent students & Graduate: higher limits, varying by program. | Low fees; interest accrues during all periods, including deferment/grace. |

| Direct PLUS Loan | Parents of dependent undergraduate students & graduate/professional students | Generally higher than Direct Loans | Covers cost of attendance minus other aid received | Higher origination fees; interest accrues during all periods. |

| Private Student Loan | Available to students with creditworthiness or a cosigner | Varies greatly depending on credit score and lender; often higher than federal loans | Varies by lender; may cover full cost of attendance or a portion | May have origination fees, prepayment penalties, and variable interest rates. Interest accrues immediately. |

| Federal Loans (Overall) | U.S. citizens or eligible non-citizens | Rates set annually by Congress; generally fixed | Vary by loan type and year in school | Generally lower fees and more flexible repayment options than private loans. |

| Private Loans (Overall) | Typically requires good credit or a creditworthy cosigner | Rates are market-driven and can be fixed or variable | Varies by lender | Often fewer borrower protections and less flexible repayment options. |

Qualitative comparison based on the article research brief. Confirm current product details in the official docs before making implementation choices.

Private Loan Landscape: What to Expect

Private student loan interest rates are set by lenders based on creditworthiness, income, and loan term, varying significantly between lenders and borrowers.

As of late 2024, private loan rates range from about 6% to 14% or higher. Borrowers with excellent credit may get rates similar to or lower than federal PLUS loans, while those with fair or poor credit face higher rates. Shopping around and comparing offers is essential.

Private lenders offer variable and fixed rates. Variable rates may start lower but can increase, making payments unpredictable. Fixed rates offer stability but may be higher initially. Choose based on your risk tolerance.

Credit Score's Impact on Private Rates

Your credit score is the most important factor for private student loan interest rates, as lenders use it to assess borrower risk. Here's how credit score ranges impact rates (as of late 2024):

Excellent Credit (750+): Borrowers with excellent credit can typically qualify for rates as low as 6-8%. This could save you thousands of dollars over the life of the loan. Good Credit (700-749): Rates generally fall between 8-10%. Fair Credit (650-699): You'll likely see rates in the 10-12% range. Poor Credit (Below 650): Rates can be 12% or higher, and you may even be denied a loan.

For example, a $10,000 loan at 6% over 10 years accrues about $1,110 in interest. At 12%, it's approximately $2,688 – a difference of over $1,500. Improving your credit score by paying bills on time, keeping credit card balances low, and checking your report for errors can significantly lower your rate.

Comparing Loan Costs: A Hypothetical Scenario

Consider a $10,000 loan over a 10-year repayment period to illustrate the cost differences between loan types, using rates from late 2024 (subject to change).

Federal Subsidized Loan (5.05%): Assuming no interest accrues while you're in school (4 years), your total interest paid over 10 years would be approximately $1,866. Federal Unsubsidized Loan (6.82%): Interest accrues from disbursement, adding to the principal. Over 10 years, you’d pay around $2,764 in interest. Private Loan (8.5% - good credit): You’d pay approximately $3,610 in interest over 10 years.

Repayment plans also affect total cost. A standard 10-year plan has the lowest total interest. Graduated plans have lower initial payments that increase, leading to more total interest. Income-driven plans for federal loans can lower monthly payments based on income and family size, but may increase total interest paid.

Refinancing: A Strategy for Lower Rates?

Refinancing student loans means taking out a new loan to pay off existing ones, aiming for a lower interest rate to save money. This is offered by private lenders and requires a good credit score and stable income.

Refinancing federal loans into private ones means losing federal protections like income-driven repayment, forbearance, and loan forgiveness programs. Weigh potential savings against the loss of these benefits.

As of late 2024, average refinance rates for borrowers with good credit range from 6.5% to 8.5%, depending on individual circumstances. Refinancing is a smart strategy for those who don’t need federal protections and can secure a significantly lower rate, but it’s not for everyone.

Amazon Products for Financial Planning

Knowledge is key to managing your finances. Here are some Amazon resources for personal finance and student loan management:

The Total Money Makeover by Dave Ramsey: A classic guide to debt elimination and financial freedom. I Will Teach You To Be Rich by Ramit Sethi: A practical, step-by-step guide to managing your money and building wealth. Broke Millennial Takes on Investing: A beginner-friendly guide to investing for young adults.

These resources can provide valuable insights and strategies for managing your student loan debt and building a secure financial future. Remember, securing student loans is just the first step – responsible financial planning is crucial for long-term success.

Essential Tools for Managing Your Student Loans

Provides a step-by-step plan for achieving financial freedom. · Covers debt reduction strategies, including the debt snowball method. · Offers guidance on budgeting, saving, and investing for long-term wealth.

This book offers a comprehensive framework for taking control of your finances and building a solid foundation for debt management.

Explains various student loan repayment options. · Details strategies for student loan forgiveness programs. · Provides practical advice for navigating the student loan landscape.

This guide specifically addresses the complexities of student loan debt, offering actionable strategies for repayment and potential forgiveness.

Includes monthly budget sheets for tracking income and expenses. · Features an expense tracker to monitor spending habits. · Serves as an undated bill organizer for managing financial obligations.

This budget planner provides a structured tool to meticulously track your income, expenses, and bills, promoting better financial oversight.

Covers a wide range of personal finance topics, from budgeting to investing. · Offers clear explanations and practical advice for beginners. · Helps readers understand concepts like credit, insurance, and retirement planning.

This book serves as an accessible introduction to personal finance, equipping you with the knowledge to make informed financial decisions.

Employs a zero-based budgeting method, assigning every dollar a job. · Offers tools for tracking spending in real-time. · Provides educational resources and community support for budgeting success.

YNAB is a powerful budgeting software that helps users gain control over their money by actively planning their spending and reducing financial stress.

As an Amazon Associate I earn from qualifying purchases. Prices may vary.

No comments yet. Be the first to share your thoughts!